rzelich

Public Storage (NYSE:PSA) is one in all solely 5 publicly traded U.S. self-storage REITs providing somewhat distinctive packages for long-term traders, who additionally desire having publicity to comparatively enticing and rising dividends.

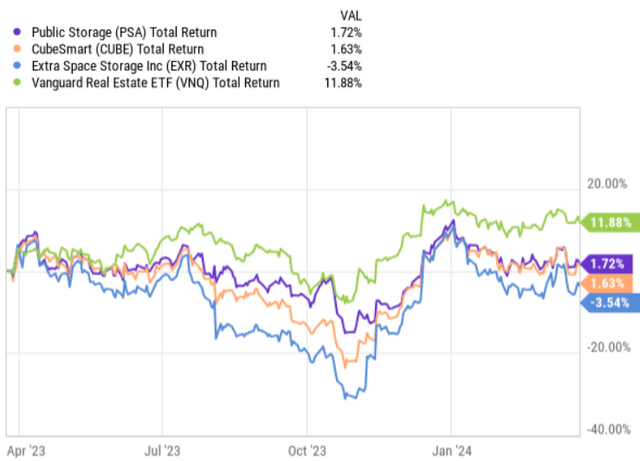

Self-storage as an asset class has traditionally outperformed the broader REIT market by a substantial margin, the place the related REIT gamers have been in a position to capitalize on the largely non-institutionalized market (i.e., small focus of property within the arms of institutional traders).

But, the previous yr has been an exception, the place the sector lastly underperformed the index.

YCharts

Whereas the Vanguard Actual Property Index Fund ETF (NYSEARCA:VNQ) has elevated by ~12%, PSA and its closest friends (with significant stability sheets) have delivered whole returns near 0% territory.

For my part, this creates an fascinating alternative to think about allocating some capital towards self-storage gamers.

Furthermore, PSA fundamentals and taking into consideration the prevailing macro-level surroundings, the thesis of going lengthy PSA appears very engaging.

Right here is why.

Thesis for going lengthy PSA

Other than the aforementioned relative underperformance that warrants an fascinating entry level in PSA, there are three distinct the explanation why it’s value contemplating opening an publicity to this REIT.

#1 Scale

At present, PSA carries the biggest market cap stage within the self-storage sector, which for this particular REIT sub-sector gives a robust benefit to ship stable outcomes going ahead.

Self-storage as an asset class requires heavier involvement from the operations crew than, for instance, within the workplace or buying heart areas. Oftentimes it’s the embedded processes and the general operational excellence that allows higher worth creation from the acquired or developed self-storage capacities.

In PSA’s case, we will see how the scale and scale have turn out to be useful by resulting in the best NOI margin ranges in the entire sector.

The margin will be improved from two parts: revenues and prices.

In relation to the revenues, a notable driver behind the enticing top-line ranges has been PSA’s geographical publicity to Southern California, which reveals sustained tailwinds, the place there are sturdy demand dynamics with restricted new provide.

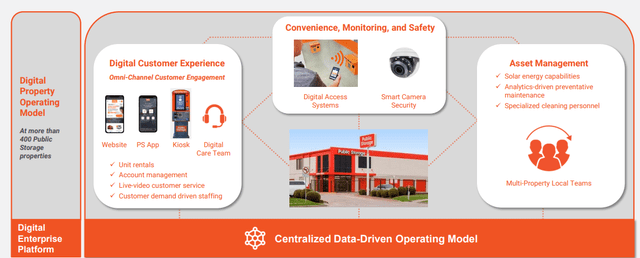

Nonetheless, the place PSA has actually taken some first rate effort (benefiting from the size) is the fee facet. Because it has greater than 3360 properties, which generate circa $3.4 billion in an annual NOI, there are ample retained money flows out there from which to make investments in centralized options.

For instance, one in all them is what’s mirrored under – the trade’s first end-to-end digital ecosystem platform.

PSA Investor Presentation

Equally, PSA has developed its personal buyer sourcing channels, digital e-rental settlement resolution, and complete app and made the entire properties accessible by way of digital options.

A part of the retained money flows have been (and are nonetheless within the pipeline) directed in the direction of utility cost-saving measures by the set up of solar energy and LED gentle options.

All of this helps hold the NOI margin excessive relative to among the smaller self-storage gamers akin to International Self Storage (NASDAQ:SELF) and Nationwide Storage Associates (NYSE:NSA) which have smaller operations and stability sheets from which to extract economies of scale. Within the operation-heavy sector like self-storage this performs a crucial function.

#2 Stable development prospects

In relation to the expansion prospects, PSA is well-positioned with two main points stimulating the FFO CAGR.

The primary is extra generic however on the similar time crucial. As I briefly talked about earlier than within the article, self-storage presents ample alternatives for institutional traders like PSA to consolidate the fragmented possession by buying items from varied smaller dimension homeowners.

On prime of this, there are much more secular tailwinds supporting the self-storage asset class: e.g., urbanization, rising e-commerce of small enterprises, and frequent relocations.

On account of this, the general asset class is ready to develop at a faster tempo than the markets through which different REITs function.

Now, if we have a look at how PSA has capitalized on these dynamics, we will clearly discover that M&A performs a significant function. That is additionally logical given the extremely fragmented area, the place the one solution to consolidate it’s by devising aggressive M&A technique.

For instance, over the last yr, PSA acquired a $2.2 billion Merely Self Storage portfolio with ca. 90,000 buyer base unfold throughout ~ 130 properties. From this, PSA managed to extend the scale of its high-growth, externally acquired pool of properties to 705, accounting roughly for 30% of the general portfolio.

These information factors actually function a testomony to PSA’s give attention to rising its presence by way of acquisitions, which is the suitable technique to assume given the above talked about market state of affairs.

Additionally it is promising to see that additionally in 2024 PSA expects to ship incremental acquisition and improvement exercise of $500 million and $450 million, respectively, thereby persevering with to increase its presence within the U.S.

Granted, the overall goal quantity of contemporary deal quantity in 2024 is smaller than in comparison with the 2023 transaction exercise. It is because the sellers are nonetheless in a “wait and see” place, holding the property to themselves till the rate of interest begin to lastly drop or at the least till the rate of interest surroundings turns into extra clear. But, the contemplating the outlined M&A pipeline for 2024 and the document quantity of redevelopment, we will nonetheless anticipate tangible development over the foreseeable future.

Let’s additionally not neglect {that a} notable chunk of incremental FFO technology (on a same-store foundation) stems from the operational excellence, which, as talked about above, goes hand in hand with the size and skill to take advantage of dimension efficiencies.

From Joe Russell – President and Chief Government Officer – commentary within the latest earnings name, we will clearly see this that the Administration places a heavy emphasis on natural development alternatives:

The complete Public Storage crew is concentrated on exercising our aggressive benefits, which embody advancing our digital and working mannequin transformation, increasing complementary companies and creating partnerships throughout the broader trade, rising the portfolio by acquisitions, improvement, redevelopment and third-party administration, and funding innovation and development in the present day and into the longer term with the trade’s greatest stability sheet.

#3 Fortress stability sheet

The ultimate main motive why, for my part, PSA is a wonderful selection for long-term traders searching for to profit from secure value appreciation at the side of significant and rising dividend in place is the stability sheet.

First, PSA is the one one amongst self-storage friends that has an higher funding grade stability sheet. For instance, its present debt ratio stands at 16.4%, which is a bit lower than 2x under the sector common.

Even after factoring in the popular shares, the Internet Debt + Most popular Fairness to EBITDA lands at 3.9x, which is materially under PSA’s mid goal vary of 4.5x.

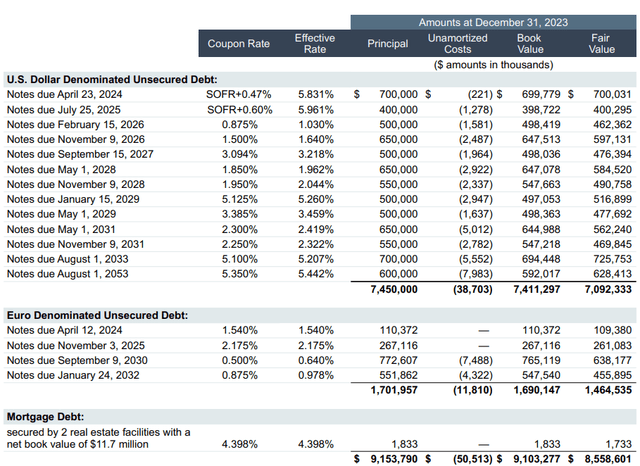

Furthermore, the underlying borrowings are structured in a somewhat favorable method, the place a lot of the maturities are back-end loaded far sooner or later. It is a actual benefit if the rates of interest are locked in at under market stage financing charges.

Right here, in PSA’s case we will see that happening, the place virtually the entire borrowings that begin to mature in 2026 and past are assumed at fastened rates of interest, that are significantly under the prevailing value of financing ranges.

PSA Investor Presentation

Having a fortress stability sheet with spare debt capability is a big benefit not solely from the danger mitigation perspective but additionally from the sustainable development angle. This enables PSA to execute the expansion agenda with out impairing its monetary profile or inflicting the price of capital to dramatically enhance.

Dangers

Now, whereas the underlying fundamentals are sturdy and the long-term tailwinds are there, we have now to understand the likelihood of dealing with additional draw back volatility in PSA’s share value.

All in all, the truth that PSA has underperformed the broader REIT market sends a sign of some relative weak spot in PSA. The principle problem is that PSA, similar to most self-storage REITs, has confronted important stress from surging enter prices, the place the highest line has not managed to extend sufficient to offset the headwinds on the fee facet. On account of this, the identical retailer NOI and FFO outcomes have most often stayed flat or elevated however at a fraction of what the market expects.

Moreover, a notable danger lies within the rate of interest path, the place if the Fed all of the sudden decides to maintain the rates of interest unchanged and assume the next for longer stance, PSA’s development prospects would undergo. Within the larger rate of interest environments, the M&A market is per definition not that enticing and energetic as within the case of actually accommodative SOFR surroundings (e.g., zero % rates of interest). For PSA that has to depend on exterior development to ship on its fairness story, such a state of affairs would possibly hold the share value flat for longer.

Nonetheless, each of those dangers embody comparatively minor likelihood ranges as, first, PSA has the best-in-class operational platform to drive efficiencies, thus safeguarding the margins (2023 FFO development of ~6% is proof of that), and, second, it’s extremely doubtless that the Fed will lower at the least two or thrice this yr that ought to stimulate the M&A market accordingly.

The underside line

Given the entire above – the basics and sector dynamics – PSA is a purchase.

The choice of setting a purchase right here is simpler if we additionally contextualize PSA’s valuations with these of the friends who’ve weaker stability sheets, smaller scales, and decrease NOI margins.

At present, PSA trades at a P/FFO of 16x, which is slightly below the sector common, despite the fact that contemplating the inherent benefits of PSA, we should always see a presence of some type of premium over the friends. The P/FFO of 16x can be ~25% under the 3-year common, which in opposition to the backdrop of lastly normalizing rates of interest and promising development prospects additional signifies a compelling entry level.

For me, PSA is a purchase.

{kind=link}