Khanchit Khirisutchalual

I’ve been following PubMatic (NASDAQ:PUBM) because the firm got here public within the second half of 2020 because it was a brand new participant in a quick rising market and was truly boasting spectacular metrics, reminiscent of very excessive gross margins, income progress and was additionally persistently worthwhile. With these traits, it did not take lengthy for the inventory to be caught within the final tail of the market bubble, and the inventory was shortly bid up 158% in February 2021. From that second, the inventory solely went down and is sitting now over 70% down from all-time highs, at a market cap simply shy of $900 million.

Nonetheless, quarter after quarter the corporate by no means dissatisfied and has truly confirmed to have the ability to continue to grow its enterprise in a sustainable method, virtually with no acquisitions whereas nonetheless sustaining each constructive GAAP internet revenue in addition to free money circulation, a really uncommon sight amongst very excessive progress corporations. With the shares declining a lot over the previous yr, I consider the valuation is greater than truthful in the mean time and an funding in PubMatic seems fairly beneficial.

Common thesis and up to date efficiency

The principle thesis round an funding in PubMatic revolves actually across the growing digitalization of promoting as a complete. The corporate operates in digital promoting, offering an infrastructure to its prospects that permits real-time programmatic promoting transactions. Co-Founder and CEO Rajeev Goel has said over the last earnings name that “all promoting will probably be digital, and all digital promoting will probably be transacted programmatically”. Whereas the assertion will in all probability not be confirmed to be precisely right (I consider there’ll all the time be part of promoting which will not be digital or programmatic), the worldwide macro pattern is indeniable and PubMatic appears effectively positioned to achieve shares of it. In 2022, round 63% of whole advert spending is estimated to be spent in direction of digital advertisements, a share that can also be estimated to develop to 73% in 2026 in response to Insider Intelligence and eMarketer.

The pattern can also be clear in Related TV (CTV) and streaming as a complete: each Disney+ and Netflix have plans to quickly introduce ad-supported tiers of their streaming providers which can additional gas the expansion of the world by which PubMatic is extra specialised. Within the final quarter, CTV income progress hit over 150% whereas omnichannel video share of whole income reached over 30%.

PubMatic Q2 2022 Earnings Report

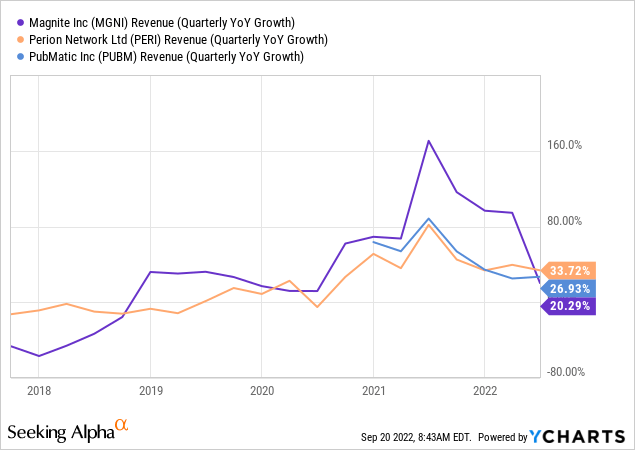

PubMatic has undoubtedly skilled a slowdown in income progress from mid-2021 onwards, according to the Federal Reserve beginning a brand new cycle of extra hawkish financial coverage and the looming of a possible arduous touchdown induced recession spelling worry for a lot of industries, promoting included. There isn’t a beating across the bush that in a recession companies usually dedicate much less of their price range to promoting and extra to, effectively, navigating the hardship. Nevertheless, as the next chart demonstrates the slowdown in income progress is completely not distinctive to PubMatic however as an alternative has hit additionally its extra direct rivals Magnite (MGNI) and Perion Community (PERI).

YCharts – Looking for Alpha

What’s nevertheless distinctive to PubMatic in comparison with the aforementioned rivals is being persistently worthwhile since going public: the final Q2 2022 was the thirteenth consecutive quarter producing constructive GAAP Internet Earnings, and likewise marked a sequential re-acceleration of income progress from 25% YoY reached in Q1 2022 to 27% YoY progress in Q2 2022.

PubMatic Q2 Earnings Report

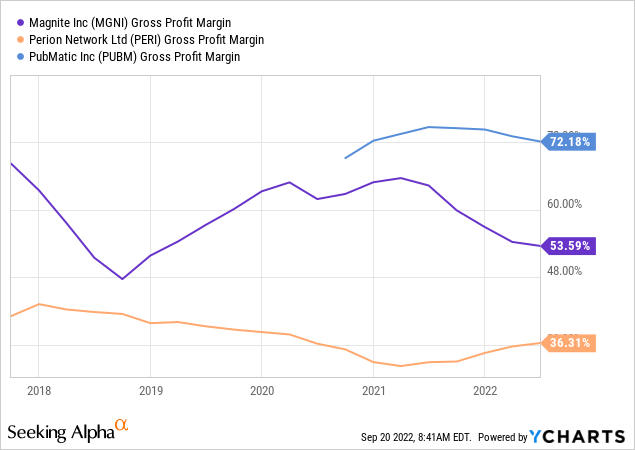

Furthermore, PubMatic can also be having fun with an impressively excessive gross revenue margin because of proudly owning and managing its personal digital infrastructure:

By proudly owning and working our infrastructure now we have been in a position to drive down our unit prices. Over the past two years, now we have diminished our value of income per million impressions processed by roughly 50%. Our expertise has proven us that the return on funding for incremental capability is excessive and sometimes pays for itself on a money foundation in months. With this value benefit, the place we see incremental income alternatives, we are going to develop our processing capability and additional enhance our aggressive moat.

YCharts, Looking for Alpha

Constructing and working the infrastructure naturally interprets into greater capital expenditures in the mean time, nevertheless that is the basic instance of quick time period ache for long run positive aspects. Administration has highlighted how the timing of sure gear purchases will look notably unfavourable within the present quarter; nevertheless, the free money circulation pattern ought to normalize sooner or later:

We anticipate CapEx between $33 million and $36 million this yr. Primarily based on timing of apparatus availability and shipments, the majority of our CapEx will happen this quarter and can cut back our free money circulation. We anticipate a return to a extra typical sample of free money circulation technology in This fall. Trying forward, as video and different excessive worth codecs develop into a better share of our income combine, and as we proceed optimizing new infrastructure, we anticipate that our CapEx to income ratio will decline.

Administration has additionally highlighted PubMatic’s Internet Income Retention Price of 130%, which means that any buyer acquired prior to now by the corporate has truly spent 30% extra this yr in comparison with the previous. This metric is well-known to buyers that observe Software program-as-a-service shares as it’s generally shared by such corporations, nevertheless it is uncommon for an promoting enterprise to retain such a excessive degree variety of prospects and likewise handle to develop their spending on the platform.

What may go incorrect

It is all the time useful to evaluation the dangers of any funding as there is no such thing as a such a factor as “risk-free”. In the beginning, PubMatic remains to be a small participant in an more and more vital and aggressive trade. Programmatic digital promoting will develop for years to come back and also will must adapt to new technological challenges such because the onset of recent mediums and even new rules. Promoting immediately is extremely totally different than 15 years in the past, and there’s a likelihood that will probably be very totally different once more in 15 years’ time. Whereas The Commerce Desk seems as of immediately as a transparent winner on the demand facet of the equation, the jury remains to be out on who’s going to be the clear winner (if any) on the availability facet. As of immediately any metric means that PubMatic is effectively positioned for working efficiently sooner or later, however something can occur. Fortunately buyers can handle this threat just by allocating a small share of their portfolio to such bets in an effort to cut back the general publicity to unsure outcomes.

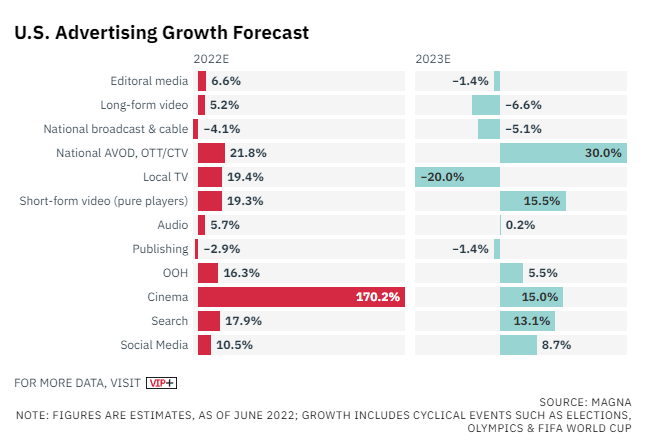

Within the quick time period there is no such thing as a doubt {that a} doable recession within the US and elsewhere will have an effect on the promoting enterprise general. We just lately had a glimpse of what may occur through the fast COVID downturn in early 2020, which had such a profound influence that international promoting spending for 2020 truly declined 4.2% in response to media funding firm Magna. Estimates for full 2022 and 2023 within the US are certainly not that rosy: whereas the midterm election ought to present a lift in 2022 by way of greater political advert spending, estimates for 2023 present numerous declines with the one brilliant spots being AVDO, OTT and CTV – PubMatic’s sturdy go well with.

Magna – Selection

In August 2022 through the newest Q2 2022 report, the corporate has already revised the total yr income steering all the way down to $277 million to $281 million (23% progress on the midpoint), citing well-known international uncertainties particularly within the Europe and APAC area reminiscent of excessive inflation, vitality disaster, the battle in Ukraine and COVID-zero coverage in China destabilizing provide chains and shopper exercise. Nonetheless, administration appears up to the mark and has already initiated cost-cutting initiatives that ought to allow full yr Adjusted EBITDA margin at round 38%. Steadiness sheet is definitely additionally very strong with $183 million of money and money equivalents and solely about $22 million of long run debt, therefore a money crunch throughout an financial downturn doesn’t seem like a difficulty for PubMatic.

Valuation and Key Takeaway

PubMatic has seen its share worth beneath stress for over 18 months now, leaving the corporate buying and selling for a really affordable valuation in my view. The corporate is at the moment buying and selling at Value to Gross sales of simply 2.84, destined to shortly get decrease on condition that Wall Avenue analysts additionally estimate about 19% income progress for 2023. With the macro setting getting higher possibly in 2024 or 2025 I would not be stunned in any respect to see PubMatic progress charge truly speed up once more along with the worldwide promoting market rebound. On the earnings facet, P/E of about 18 is affordable in contrast of PERI’s P/E of 14 whereas MGNI has no GAAP internet revenue to check but. A slight premium for PubMatic based mostly on a lot greater gross margins as said above and strong stability sheet is a suitable worth to pay.

I consider on the present worth PubMatic has the potential to ship long run progress assuming will probably be in a position to persistently ship as achieved prior to now. I’d nonetheless not allocate a big portion of my portfolio to the corporate as its dimension nonetheless provides appreciable threat; nevertheless, a average method by averaging down if the value will hold falling could possibly be a profitable technique till reaching full allocation dimension.

{kind=link}