Employer- and union-sponsored retiree well being advantages have served as an vital supply of supplemental protection for folks on Medicare. Retiree well being plans have helped fill the gaps in Medicare’s profit design by filling in some or all of Medicare’s deductibles and cost-sharing necessities and providing advantages that aren’t coated by conventional Medicare, equivalent to dental and imaginative and prescient and a cap on out-of-pocket spending.

For the previous 25 years, KFF has tracked traits in employer-sponsored protection, together with retiree well being advantages. KFF’s 2023 employer survey exhibits a drop within the share of huge employers (with 200 or extra workers) providing well being advantages to their retirees from 29% in 2020 to 21% in 2023, down from 66% in 1988. Amongst massive employers that also supply retiree well being advantages to Medicare-age retirees, KFF’s survey reveals a considerable rise within the share doing so by way of Medicare Benefit plans in recent times. As we speak, about 5 million Medicare-age retirees get their Medicare and supplemental retiree advantages from a bunch Medicare Benefit plan, in accordance with KFF’s separate evaluation of Medicare Benefit enrollment knowledge.

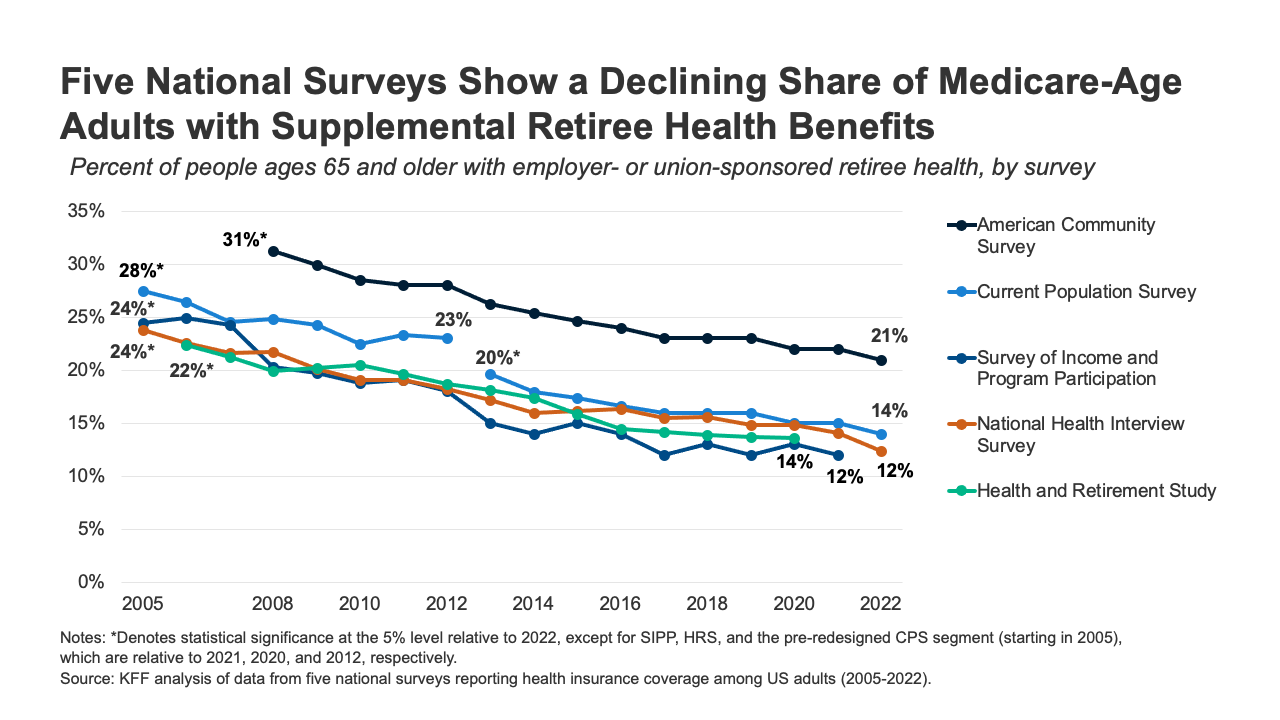

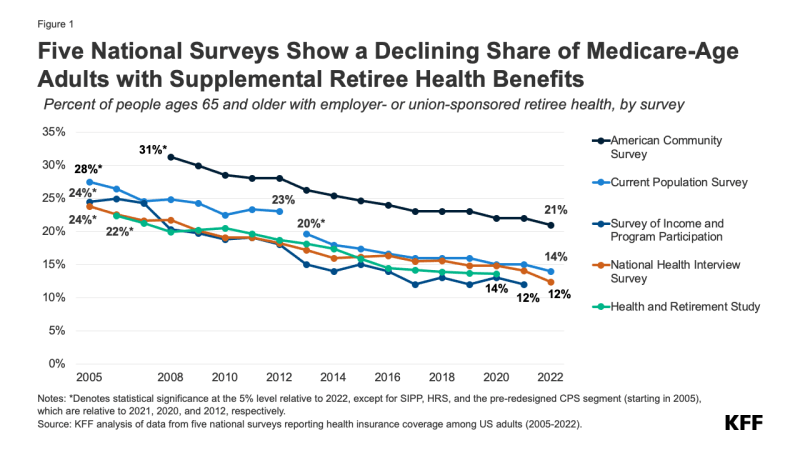

This knowledge word analyzes 5 nationwide surveys to evaluate traits in retiree well being protection amongst folks ages 65 and older (Determine 1). These 5 surveys produce considerably completely different estimates of retiree well being protection, however collectively paint a transparent image: the share of Medicare-age adults with employer- or union-sponsored retiree well being protection has been shrinking and seems to be on the way in which to extinction.

Estimates of the share of individuals ages 65 and older with retiree well being advantages in 2022 range throughout the 5 surveys, starting from 21% (American Neighborhood Survey) to 12% (Nationwide Well being Interview Survey). These variations are probably resulting from variations in pattern measurement, variations in query wording, skip patterns and pattern inhabitants (See Strategies). As with the estimates for 2022, the pattern traces additionally range. For instance, the American Neighborhood Survey exhibits the share declining from 31% in 2008, whereas the Nationwide Well being Interview Survey exhibits the share declining from 22% in 2008 that yr.

Retiree well being advantages look like heading towards extinction for numerous causes. The rise in well being care prices has put stress on employers to make tradeoffs between offering advantages to energetic staff versus retirees, accelerating this pattern. Union membership has steadily declined over the previous few a long time, easing the stress on employers to offer retiree advantages. And the demand for retiree advantages could also be much less intense than it as soon as was as a result of Medicare advantages have improved considerably through the years, with the prescription drug profit that was added in 2006 and the supply of some further advantages for beneficiaries who select to enroll in a Medicare Benefit plan.

The erosion of retiree well being protection, given the excessive price of well being care and the modest incomes and property of a giant share of the Medicare inhabitants, heightens the significance of Medicare protection selections for retiring boomers and their spouses, and the significance of addressing the challenges going through Medicare’s future. Throughout every of those nationwide surveys, retiree advantages appear to be going, going and will quickly be gone.

Strategies

This knowledge word relies on an evaluation of 5 nationwide surveys. The evaluation of the Present Inhabitants Survey can’t be trended to years previous to 2013 resulting from enhancements made by the U.S. Census Bureau to the Well being Insurance coverage Questionnaire of the Present Inhabitants Survey between 2012 and 2013. This evaluation doesn’t embody knowledge from the Medicare Present Beneficiary Survey resulting from methodological modifications which can be prone to affect protection task and traits.

Variations reported within the paper and within the determine denote statistical significance on the 5% stage relative to 2022, apart from SIPP, HRS, and the pre-redesigned CPS phase (beginning in 2005), that are relative to 2021, 2020, and 2012, respectively. The numbers displayed present the p.c of retired folks ages 65 and older who’re holding employer-sponsored insurance coverage (ESI) from any supply, apart from these within the ACS, which depicts the p.c of individuals ages 65 and older not within the labor pressure who’re holding ESI from any supply.

All surveys present annual estimates, apart from SIPP, which offers knowledge month-to-month; all depicted SIPP knowledge are from September of the given yr. HRS knowledge are supplied each two years (even-numbered years).

Tricia Neuman is with KFF. Anthony Damico is an unbiased marketing consultant.

{kind=link}