Olivier Le Moal

Focus of Article:

The main target of PART 1 of this text is to research Rithm Capital Corp.’s (NYSE:RITM) current outcomes and examine a number of of the corporate’s metrics to 19 mortgage actual property funding belief (mREIT) friends. This evaluation will present previous and present information with supporting documentation inside 4 tables. Desk 1a will examine RITM’s funding composition, current leverage, hedging protection ratio, and alter in funding portfolio dimension to the 19 mREIT friends. Desk 1b will examine RITM’s BV, financial return (loss), and premium (low cost) to estimated CURRENT BV utilizing inventory costs as of three/15/2024 to the 19 mREIT friends. Desk 2a will present an summary of RITM’s funding portfolio, Desk 2b will present a portfolio overview of RITM’s lately closed acquisition of Sculptor Capital Administration Inc. (“SCU”), and Desk 2c will present some particulars relating to the corporate’s largest present driver of earnings, its mortgage servicing rights (“MSR”) sub-portfolio. Desk 3 will present RITM’s current hedging protection ratio over the prior 5 quarters (solely contributor/crew to offer steady detailed hedging metrics).

I’m scripting this 2-part article as a result of requests that such an evaluation be particularly carried out on RITM versus its mREIT friends at periodic intervals. This text additionally discusses the significance of understanding the composition of RITM’s funding and derivatives portfolios relating to projecting the corporate’s future quarterly outcomes as rates of interest/yields fluctuate. Understanding the traits of an organization’s funding and derivatives portfolios can shed some mild on which firms are overvalued or undervalued strictly per a “numbers” evaluation. This isn’t the one information that ought to be examined to provoke a place inside a specific inventory/sector. Nevertheless, I consider this evaluation is an effective “starting-point” to start a dialogue on the subject.

On the finish of this text, there will probably be a conclusion relating to the next comparisons between RITM and the 19 mREIT friends: 1) trailing 24-month financial return (loss); 2) leverage as of 12/31/2023; 3) hedging protection ratio as of 12/31/2023; and 4) premium (low cost) to my estimated CURRENT BV (BV as of three/15/2024). My BUY, SELL, or HOLD suggestion and up to date worth goal for RITM will probably be within the “Conclusions Drawn” part of this text. This contains offering an inventory of the mREIT shares I presently consider are undervalued (a purchase suggestion), overvalued (a promote suggestion), or appropriately valued (a maintain suggestion).

Overview of A number of Classifications throughout the mREIT Sector:

I consider there are a number of completely different classifications with regards to mREIT firms. For functions of this text, I’m specializing in 4. It ought to be famous in mild of a number of prior acquisitions and sure adjustments in general funding methods, some mREIT firms have minor-modest sub-portfolios exterior every entity’s foremost focus. Nevertheless, I’ve continued to group sure mREIT firms in every entity’s foremost classification for functions of this text. Some market contributors (and even some mREIT firms) have completely different classifications when in comparison with Desk 1a. Some market contributors/firms base classifications on the share of capital deployed in every entity’s funding portfolio. Nevertheless, my desire is to base an organization’s classification on the financial “truthful market worth” (“FMV”) of every underlying portfolio which, in truth, is what drives valuation fluctuations. In my skilled opinion, there isn’t a “uniform” methodology with regards to classifying mREIT firms however extra of an underlying desire. Readers ought to perceive this because the evaluation is introduced beneath.

First, there are mREIT firms that earn a majority of revenue from investing in fixed-rate company mortgage-backed securities (“MBS”). These investments consist of economic/residential MBS, collateralized mortgage obligations (“CMO”), and company debentures for which the principal and curiosity funds are assured by government-sponsored enterprises/entities (“GSE”). That is extraordinarily vital to grasp (particularly when markets incorrectly priced on this notion on the onset of COVID-19 in early 2020). Since these investments usually have increased durations versus most different investments throughout the broader mREIT sector, firms inside this classification usually make the most of increased hedging protection ratios in occasions of rising mortgage rates of interest/U.S. Treasury yields (or a projected rise over the foreseeable future). AGNC Funding (AGNC), ARMOUR Residential REIT (ARR), Cherry Hill Mortgage Funding (CHMI), Dynex Capital (DX), Invesco Mortgage Capital (IVR), Annaly Capital Administration (NLY), Orchid Island Capital (ORC), and Two Harbors Funding (TWO) are presently categorized as a fixed-rate company mREIT. Out of those 8 company mREITs, CHMI and TWO presently have a big mortgage servicing rights (“MSR”) sub-portfolio as nicely.

Second, there are mREIT firms that earn various parts of revenue from investing in company MBS holdings, non-agency MBS holdings, different securitizations, and non-securitized mortgage-related debt and fairness investments (together with residential/industrial loans). The sort of firm is named a “hybrid” mREIT. With reference to non-agency MBS, this contains (however shouldn’t be restricted to) Alt-A, prime, subprime, and re/non-performing loans the place the principal and curiosity are not assured by a GSE. Since there isn’t a “authorities assure” on the precept or curiosity funds of non-agency MBS and residential/industrial loans (or rental revenue on properties), coupons are typically increased when in comparison with company MBS of comparable maturity. Nevertheless, borrowing prices (together with repurchase agreements) for these particular investments are additionally increased (no authorities assure; credit score danger). Because of the refined but identifiable variations between company MBS, non-agency MBS, and residential/industrial loans, I wish to differentiate between an company and a hybrid mREIT firm. Since there may be credit score danger with regards to non-agency MBS and residential/industrial loans, leverage ratios are usually decrease when investing in these securitizations/investments when in comparison with company MBS (even when credit score danger stays low). Chimera Funding Corp. (CIM), Ellington Monetary Inc. (EFC) (transformed to a REIT in 2019), MFA Monetary (MFA), AG Mortgage Funding Belief (MITT), New York Mortgage Belief (NYMT), and Prepared Capital (RC) are presently categorized as a hybrid mREIT. It ought to be famous RC was moved from an originator and servicer mREIT to a hybrid mREIT in the course of the fourth quarter of 2023 because of the firm’s quickly declining proportion of paycheck safety program (“PPP”) loans (which the corporate additionally providers) immediately because of the COVID-19 pandemic.

Third, there are mREIT firms that spend money on however aren’t restricted to, a mix of company MBS, non-agency MBS, credit score danger transfers (“CRT”), different mortgage-related investments, non-securitized debt investments (together with residential, multifamily, and industrial loans), and MSRs. There are additionally mREIT firms which have underlying subsidiaries that immediately originate mortgages (together with through correspondent manufacturing) and/or mortgage-related debt merchandise. I presently consider RITM and PennyMac Mortgage Funding Belief (PMT) ought to be categorized as an “originator and servicer” mREIT. Since RITM and PMT presently have not less than a modest portion of the corporate’s funding portfolio in MSR and MSR-related investments, which act as an “oblique” hedge (the identical may be mentioned relating to curiosity solely [IO] securities), these firms don’t must make the most of as excessive of a hedging protection ratio when in comparison with the company mREIT sub-sector (some may even argue to not have by-product devices in place; if something, “contra” hedges to counter a drop in charges/yields). Oblique hedges aren’t calculated inside every firm’s hedging protection ratio inside this evaluation (not the primary goal of those investments). As I’ve identified prior to now, these investments truly profit, from a valuation standpoint, in a rising rate of interest setting as prepayment danger (and in a majority of eventualities credit score danger) decreases whereas there is a rise in projected future discounted money flows (and vice versa).

Lastly, there are mREIT firms that mainly solely spend money on non-securitized, industrial entire loans with underlying collateral (actual property) tied to workplaces, multifamily items, accommodations, retail shops, industrial complexes, and different miscellaneous varieties of properties. Relating to the 4 industrial entire mortgage mREIT friends I presently cowl, Ares Business Actual Property Corp. (ACRE), Blackstone Mortgage Belief, Inc. (BXMT), Franklin BSP Realty Belief, Inc. (FBRT), and Granite Level Mortgage Belief Inc. (GPMT), these firms usually originate/spend money on variable-rate, interest-only senior secured (usually first lien) debt. Since ACRE, BXMT, FBRT, and GPMT all had 98%+ of their funding portfolio in variable-rate debt as of 12/31/2023, these firms presently don’t must make the most of a excessive hedging protection ratio (some may even argue to not have by-product devices in place; LIBOR/SOFR flooring are substitute as nicely).

Now allow us to begin the comparative evaluation between RITM and the 19 mREIT friends.

Leverage, Hedging Protection Ratio, BV, Financial Return (Loss), and Premium (Low cost) to Estimated Present BV Evaluation – Overview:

Allow us to begin this evaluation by first getting accustomed to the knowledge offered in Desk 1a and 1b beneath. This will probably be useful when explaining how RITM compares to the 19 mREIT friends in regard to the metrics acknowledged earlier.

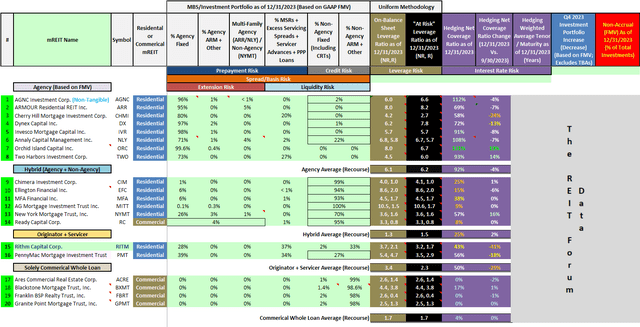

Desk 1a – mREIT Asset Composition, Leverage, Hedging Protection Ratio, and Change in Funding Portfolio Dimension

The REIT Discussion board

Desk 1a above offers the next data on RITM and the 19 mREIT friends (see every corresponding column): 1) generalized MBS/funding portfolio composition as of 12/31/2023; 2) on-balance sheet leverage ratio as of 12/31/2023; 3) at-risk (complete) leverage ratio as of 12/31/2023; 4) hedging protection ratio as of 12/31/2023; 5) quarterly change in hedging protection ratio (12/31/2023 versus 6/30/2023); 6) hedging weighted common tenor/maturity; 7) change in funding portfolio dimension (excludes off-balance sheet transactions); and 8) non-accrual proportion of sure choose mREIT friends as of 12/31/2023 (specifically all industrial entire mortgage friends, MITT, and RC). Some readers might discover some mREIT friends have “two units” of leverage ratios inside one shade set. That is because of the reality I escape each non-recourse and recourse leverage. Throughout the two units of leverage ratios inside one column, recourse leverage ratios are represented by the decrease determine on the right-hand facet and are deemed extra vital.

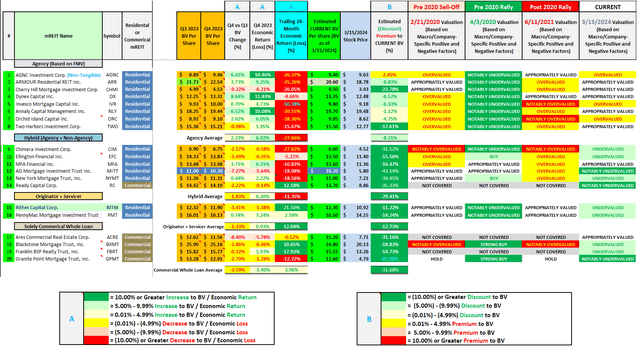

Desk 1b – BV, Financial Return (Loss), and Premium (Low cost) to Estimated Present BV Evaluation

The REIT Discussion board

Desk 1b above offers the next data on RITM and the 19 mREIT friends (see every corresponding column): 1) BV per share on the finish of the third quarter of 2023; 2) BV per share on the finish of the fourth quarter of 2023; 3) BV per share change in the course of the fourth quarter of 2023 (proportion); 4) financial return (loss) (change in BV and dividends accrued for/paid) in the course of the fourth quarter of 2023 (proportion); 5) financial return (loss) in the course of the trailing 24-months (proportion); 6) my estimated CURRENT BV per share (BV as of three/15/2024); 7) inventory worth as of three/15/2024; 8) 3/15/2024 premium (low cost) to my estimated CURRENT BV (proportion); 9) 2/21/2020 valuation evaluation (pre market sell-off as a result of coronavirus [COVID-19]); 10) 4/3/2020 valuation evaluation (publish majority of market sell-off as a result of COVID-19); 11) 6/11/2021 valuation evaluation (publish majority of market rally as a result of COVID-19 epidemic and previous to extra “hawkish” rate of interest and financial coverage rhetoric); and 12) 3/15/2024 valuation evaluation.

Evaluation of RITM:

Utilizing Desk 1a above as a reference, as of 12/31/2023 RITM’s funding portfolio consisted of 28% and 0% fixed- and variable-rate company MBS, respectively (primarily based on FMV). When in comparison with 9/30/2023, RITM’s proportion of fixed- and variable-rate company MBS remained unchanged. RITM additionally had 37% allotted to MSR investments. When calculated, this sub-sector decreased (1%). Lastly, RITM continued to spend money on non-agency MBS and non-MBS holdings (primarily mortgage-related residential entire loans) which accounted for 35% of the corporate’s funding portfolio stability as of 12/31/2023. When calculated, this mixed sub-sector elevated 1%. When damaged out, as will probably be proven in Desk 2a in a bit, this sub-sector included however was not restricted to, RITM’s investments in residential entire loans, single-family leases (“SFR”), shopper finance loans, industrial actual property (very minor proportion), and different miscellaneous mortgage-related investments.

When excluding borrowings collateralized by property held in “securitization trusts” (non-recourse debt), RITM had an on-balance sheet leverage ratio of two.1x whereas the corporate’s at-risk (complete) leverage ratio, when together with its off-balance sheet web (brief) “to-be-announced” (“TBA”) MBS place, was 1.7x as of 12/31/2023. RITM had an on-balance sheet and at-risk (complete) leverage ratio of two.1x and 1.5x as of 9/30/2023, respectively. As such, RITM maintained the corporate’s on-balance sheet leverage whereas very barely rising its at-risk (complete) leverage in the course of the fourth quarter of 2023. This was primarily as a result of a really minor improve in RITM’s on-balance sheet funding portfolio dimension and a slight lower within the firm’s web (brief) TBA MBS place in the course of the quarter. As of 12/31/2023, RITM continued to have a decrease at-risk (complete) leverage ratio when in comparison with the opposite originator + servicer mREIT sub-sector peer inside this evaluation, PMT.

Shifting on, utilizing Desk 1b above as a reference, RITM had a BV of $12.32 per widespread share on the finish of the third quarter of 2023. RITM had a BV of $11.90 per widespread share on the finish of the fourth quarter of 2023. This calculates to a quarterly BV lower of (3.41%). When together with RITM’s quarterly dividend of $0.25 per widespread share, the corporate had an financial lack of (1.38%) for the fourth quarter of 2023. RITM’s quarterly BV and financial loss was primarily the results of the short, sharp lower in mortgage rates of interest/U.S. Treasury yields in the course of the fourth quarter of 2023. Merely put, as I accurately anticipated, RITM recorded a proportionately massive quarterly lower within the valuation of the corporate’s MSR sub-portfolio. A notably extra detailed earnings evaluation article was beforehand offered to Investing Group subscribers. In actual fact, all 20 mREIT earnings outcomes had been beforehand mentioned with Investing Group subscribers in “actual time” by earnings chat notes and subsequent evaluation articles.

Even when factoring in RITM’s BV lower in the course of the fourth quarter of 2023, not like mainly all different mREIT sub-sector friends, RITM has truly been in a position to develop the corporate’s BV over the prior 2 years or in order mortgage rates of interest/U.S. Treasury yields have shortly web risen. This has led to a notable financial return outperformance for RITM. In actual fact, RITM’s trailing 24-month financial return of 21.50% is a 3.57% outperformance when in comparison with the second finest mREIT peer performer FBRT, at 17.93%. In shut comparability, PMT has reported a trailing 24-month financial return of solely 2.58%. Merely put, RITM has notably outperformed each the corporate’s sub-sector and broader sector friends over the previous 2 years relating to each BV fluctuations and financial returns. This notable outperformance ought to be seen as a constructive catalyst/pattern that markets proceed to not totally consider relating to RITM’s inventory worth when in comparison with friends.

To grasp RITM’s current financial return dominance, it is very important have a fundamental understanding of what the corporate invests in and the way it’s completely different when in comparison with most broader mREIT sector friends. Desk 1a above offered start line for this distinction. Nevertheless, allow us to now additional focus on RITM’s funding and derivatives portfolios to identify sure traits which have impacted (and can affect future) outcomes. Desk 2a beneath offers an summary of RITM’s current funding portfolio.

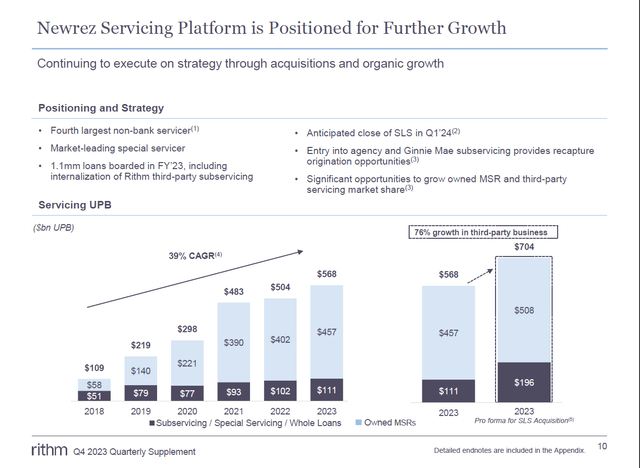

Desk 2a – RITM Current Funding Portfolio Overview

RITM Q3 2023 Shareholder Presentation

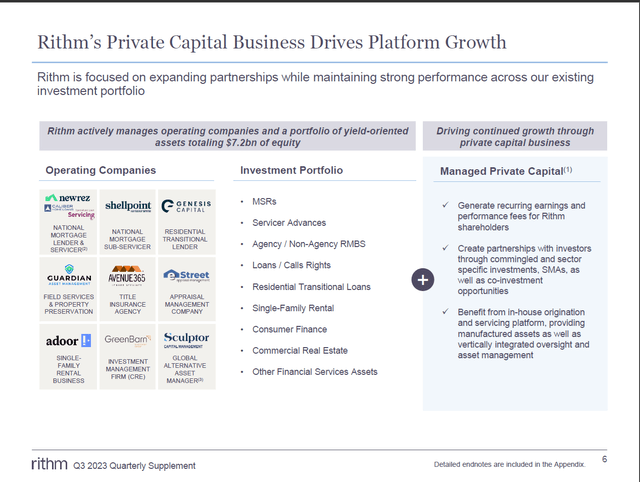

Utilizing Desk 2a above as a reference, RITM’s funding portfolio consists of the next: 1) MSRs; 2) servicer advances (immediately associated to MSRs); 3) company/non-agency residential MBS; 4) residential entire loans (together with sure name rights on mentioned loans); 5) residential transitional/bridge loans; 6) SFR; 7) shopper finance loans; 8) industrial actual property loans; and 9) different monetary servicing-related property. This desk additionally offers the relevant underlying subsidiary(ies) for every sub-portfolio. Merely put, when in comparison with say a typical company mREIT peer, RITM has a wide selection of economic investments. This added diversification immediately ends in “pure hedges” which truly act as a “contra-hedge” versus the company mREIT sector. As an illustration, when mortgage rates of interest/U.S. Treasury yields web improve, typically all company mREIT sub-sector friends usually expertise BV decreases over a chronic time period. This turns into very true when unfold/foundation danger spikes (as we lately noticed earlier this yr). That is because of the reality the worth of long-term, fixed-rate company MBS costs lower which is simply partially mitigated by associated hedging/by-product devices. Nevertheless, inside RITM’s funding portfolio, the corporate has allotted a notable proportion of capital to MSR and MSR-related property. As extensively mentioned prior to now, primarily by our Investing Group, MSR and MSR-related property usually achieve in worth when mortgage rates of interest/U.S. Treasury yields web improve.

After all, totally modeling out valuation fluctuations inside every of RITM’s sub-portfolios is far more concerned versus this fundamental assertion (once more, one thing we do on the subscriber facet) however readers ought to get the fundamental “gist” of this relationship for functions of this sector comparability article. Desk 2a is solely offering a fundamental understanding of the underlying working firms which might be owned/managed by RITM. This contains, however shouldn’t be restricted to, 9 current underlying subsidiaries, 1 lately closed acquisition, SCU, and 1 soon-to-be finalized acquisition, Specialised Mortgage Servicing LLC (“SLS”). Once more, the important thing level right here is sustained acquisitions inside core enterprise operations (MSR-related investments relating to SLS) and broadening diversification inside new funding alternatives (amongst different investments, one other asset supervisor with SCU).

Desk 2b – SCU Asset Administration Overview

RITM This fall 2023 Shareholder Presentation

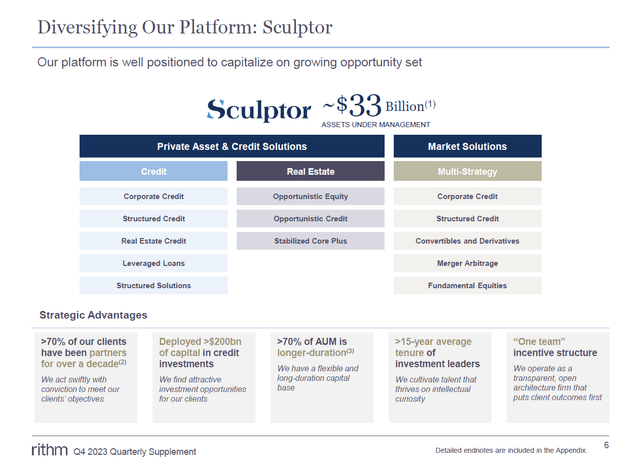

Utilizing Desk 2b above as a reference, RITM’s acquisition of SCU instantly brings roughly $33 billion of investments below administration. This contains investments throughout the following: 1) company credit score; 2) structured credit score; 3) actual property credit score; 4) leveraged loans; 5) structured options; 6) opportunist debt and fairness investments inside actual property; and 7) strategic investments in a number of varieties of monetary devices. Merely put, a typical theme with RITM, diversification (a “ramp up” of asset administration providers) and economies of scale to drive future development and returns.

Whereas RITM continues to have a various array of underlying subsidiaries and funding segments, one of many firm’s foremost drivers of BV fluctuations and earnings stays its MSR and MSR-related investments. As such, allow us to take a fast have a look at RITM’s MSR sub-portfolio through Desk 2c beneath.

Desk 2c – RITM MSR Sub-Portfolio Overview

RITM This fall 2023 Shareholder Presentation

Utilizing Desk 2c above as a reference, allow us to present an summary of some key metrics relating to this sub-portfolio. RITM’s MSR sub-portfolio consisted of an underlying unpaid principal stability (“UPB”) of $568 billion as of 12/31/2023. When together with the soon-to-be-closed acquisition of SLS, RITM’s pro-forma MSR sub-portfolio would have had an underlying UPB of $704 million as of 12/31/2023. As well as, RITM’s servicing price per mortgage decreased from $134 in the course of the third quarter of 2023 to $113 in the course of the fourth quarter of 2023. Merely put, a pretty quarterly lower which may be very possible the results of continued technological enhancements inside RITM’s origination/servicing platform. RITM continues to be on the forefront on this regard. Shifting to credit score metrics, RITM’s MSRs had a 60-day+ delinquency price of two.1% in the course of the fourth quarter of 2023. When calculated, this was a (0.1%) lower when in comparison with the third quarter of 2023. These percentages stay close to current historic lows. To stay non-bias, I anticipate a minor – modest “uptick” in delinquency charges over the foreseeable future (2024 – 2025) however nothing overly “alarming”; even when the financial system strikes into a light recession. That is already factored into our modeling, per share suggestion ranges, and danger ranking. Additional evaluation of RITM’s underlying funding sub-portfolios is exterior the scope of this explicit sector comparability article (and offered inside our Investing Group).

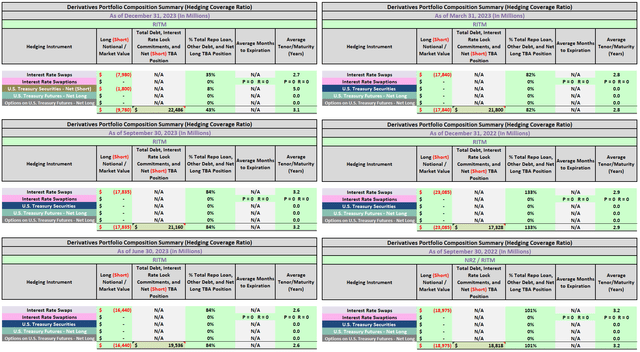

Shifting on, to spotlight the current exercise inside RITM’s derivatives portfolio, Desk 3 is introduced beneath.

Desk 3 – RITM Hedging Protection Ratio (As of 12/31/2023 Versus Prior 5 Quarters)

The REIT Discussion board

Since one in every of RITM’s foremost investments is MSR and MSR-related property, the corporate additionally invests in fixed-rate company MBS which acts as a pure hedge to mentioned investments. Nevertheless, to take RITM’s derivatives/hedging technique one step additional, to additional fight rate of interest/unfold danger inherently related to fixed-rate company MBS, the corporate additionally makes use of rate of interest payer swaps and web (brief) TBA MBS investments. Through the fourth quarter of 2023, RITM added a minor quantity of web (brief) U.S. Treasury securities.

Utilizing Desk 3 above as a reference, RITM had a web (brief) rate of interest swaps place of ($17.8) billion as of 9/30/2023. When calculated, RITM’s hedging protection ratio remained unchanged at 84% as of 9/30/2023 versus 84% as of 6/30/2023. RITM had a web (brief) rate of interest swaps and U.S. Treasury securities place of ($8.0) and ($1.8) billion as of 12/31/2023, respectively. When calculated, primarily because of the massive lower in RITM’s rate of interest payer swaps place (which mitigated some further BV erosion in the course of the fourth quarter of 2023), the corporate’s hedging protection ratio decreased to 43% as of 12/31/2023.

Shifting on, as soon as once more utilizing Desk 1b above as a reference, as of three/15/2024 RITM’s inventory worth traded at $10.92 per share. When calculated, RITM’s inventory worth was buying and selling at an (11.22%) low cost to my estimated CURRENT BV (BV as of three/15/2024; $12.30 per widespread share). Merely put, RITM’s inventory worth traded at a notable (better than a ten%) low cost to my estimated CURRENT BV and at a barely much less engaging valuation when in comparison with PMT. I proceed to consider RITM “deserves” to commerce at a barely – modestly increased valuation when in comparison with the corporate’s closest sub-sector peer, PMT, and a modestly increased valuation when in comparison with most broader sector mREIT friends.

I consider the trailing 24-month complete financial return (loss) metric is a superb instrument for recognizing every mREIT’s historic efficiency. An ideal instrument when additionally contemplating future common expectations versus friends. As such, as acknowledged later within the article, I presently consider RITM is undervalued (a BUY suggestion) from a inventory worth perspective.

Comparability of RITM’s Current Financial Return (Loss), Leverage, Hedging Protection Ratio, and Valuation to 19 mREIT Friends in Rating Order:

The REIT Discussion board Characteristic

Conclusions Drawn (PART 1):

PART 1 of this text has analyzed RITM and 19 mREIT friends regarding the following metrics: 1) trailing 24-month financial return (loss); 2) leverage as of 12/31/2023; 3) hedging protection ratio as of 12/31/2023; and 4) premium (low cost) to my estimated CURRENT BV.

First, RITM’s trailing 24-month financial return of 21.50% was a notable outperformance versus mainly all lined mREIT friends (each sub-sector and broader sector friends). For instance, the company, hybrid, originator + servicer, and industrial entire mortgage trailing 24-month financial return (loss) common was (27.66%), (11.35%), 12.04%, and three.96%, respectively. Particularly, RITM notably outperformed the corporate’s closest sector peer, PMT, by a whopping 18.92%. This was primarily because of the current composition of RITM’s funding and derivatives portfolio and the web motion of mortgage rates of interest/U.S. Treasury yields throughout this timeframe. Extraordinarily detailed reasoning of RITM’s current notable financial return outperformance was offered in quarterly earnings evaluation articles (Investing Group characteristic).

Second, RITM’s at-risk (complete) leverage as of 12/31/2023 was beneath each the originator + servicer sub-sector and broader mREIT sector common. RITM usually runs beneath common leverage versus the corporate’s closest sector peer, PMT, and company mREIT friends when wanting again a number of years. This helps fight BV volatility.

Third, RITM’s hedging protection ratio moved beneath the originator + servicer mREIT common as of 12/31/2023. This helped alleviate a extra extreme BV lower in the course of the fourth quarter of 2023. As well as, RITM continues to make the most of web lengthy fixed-rate company MBS in case mortgage rates of interest/U.S. Treasury yields web lower over the foreseeable future. That is not represented in RITM’s hedging protection ratio to keep up a constant, sector-wide metric however is tracked individually inside one other model of the ratio. Merely put, RITM stays nicely diversified (and lately has diversified much more) to ship engaging risk-adjusted returns over a number of rate of interest eventualities. That mentioned, to stay non-bias, RITM ought to be thought-about extra of a “contra mREIT play”. RITM usually notably outperforms most (if not all) broader sector friends in a rising/elevated rate of interest setting however will gravitate in the direction of sector averages when mortgage rates of interest/U.S. Treasury yields web lower to, in any case, a modest extent.

Lastly, RITM’s present valuation, when in comparison with my estimate of every mREIT’s CURRENT BV (BV as of three/15/2024), was barely much less attractively valued when in comparison with PMT. Nevertheless, by the metrics offered inside this two-part sector comparability article (together with elements/metrics in a roundabout way mentioned), I consider RITM “deserves” to commerce at a premium valuation versus mainly all mREIT friends (together with PMT). As such, this is among the the reason why I consider RITM is presently undervalued. I’d strongly counsel readers take into account CURRENT BVs (versus prior interval BVs) when assessing whether or not a inventory is attractively valued or not (accessible to Investing Group subscribers on a weekly foundation).

Relying upon the metrics specified by the tables above, outcomes throughout the broader mREIT sector will barely – notably range from peer-to-peer; dependent upon particular asset classifications and danger administration methods put into place. The connection between MBS/funding pricing and by-product instrument valuations must be continuously monitored (which I frequently carry out all through the quarter).

Shifting ahead, the prior Caliber Houses and Genesis acquisitions will proceed to profit RITM as an entire. The identical holds true relating to RITM’s more moderen partial fairness stake in GreenBarn, a subsidiary targeted on investments in industrial actual property (once more, pondering longer-term right here). As such, RITM continues to diversify the enterprise mannequin into areas exterior residential mortgages and mortgage-related investments. Relating to RITM’s current acquisition of SCU, I consider RITM has now acquired a globally-recognized asset supervisor at a really engaging valuation when contemplating longer-term prospects. Relating to RITM’s soon-to-be acquisition of SLS, that is proper within the firm’s “ballpark” per se; MSRs and associated property (together with an origination servicing enterprise). As acknowledged on the time this acquisition was first introduced, I consider this was a smart move by RITM. The SLS acquisition equates to ~10% of RITM’s complete shareholder’s fairness as of 12/31/2023.

Administration stays within the strategy of “spinning-off” the mortgage origination/servicing enterprise (together with, however not essentially restricted to, NewRez/Caliber/Shellpoint). This has been mentioned, at size, inside our Investing Group beginning again in 2020 – 2021. The “worth unlocking” of those sub-portfolios, by spinning off a number of subsidiaries, forming a brand new entity, and taking it public (present RITM shareholders would theoretically personal shares within the newly-formed public entity), can be a constructive catalyst/pattern. This chance has been constructed into our bifurcated modeling for RITM since 2019 (separate BVs). As such, this whole idea has already been considered relating to RITM’s proportion suggestion ranges, danger ranking, and worth goal.

My BUY, SELL, or HOLD Suggestion:

From the evaluation offered above (utilizing Desk 1b as a direct reference), together with further catalysts/issue not mentioned inside this text, I presently price RITM as a SELL after I consider the corporate’s inventory worth is buying and selling at or better than a 5% premium to my projected CURRENT BV (BV as of three/15/2024; $12.30 per share), a HOLD when buying and selling at lower than a 5% premium by lower than a (7.5%) low cost to my projected CURRENT BV, and a BUY when buying and selling at or better than a (7.5%) low cost to my projected CURRENT BV.

Subsequently, I presently price RITM as UNDERVALUED from a inventory worth perspective.

As such, I presently consider RITM is a BUY suggestion.

Nevertheless, to stay non-bias, I/we had a NOTABLY UNDERVALUED classification (STRONG BUY suggestion) on RITM (and many of the broader mREIT sector) in early 2023 which shortly “paid off” to readers/subscribers who deeded our recommendation with the current rally. So, presently some good worth with RITM however technically, sure, not as nice of worth versus early 2023.

My present worth goal for RITM is roughly $12.90 per widespread share. That is presently the worth the place my suggestion would change to OVERVALUED/a SELL suggestion. The present worth the place my classification/suggestion would change to APPROPRIATELY VALUED/a HOLD suggestion is roughly $11.40 per widespread share. Put one other means, the next are my CURRENT BUY, SELL, or HOLD per share suggestion ranges (subscribers get the sort of information on all 20 mREIT shares I presently cowl on a weekly foundation):

$12.90 per share or above = SELL

$11.41 – $12.89 per share = HOLD

$9.86 – $11.40 per share = BUY

$9.85 per share or beneath = STRONG BUY

Together with the info introduced inside this text, this suggestion considers the next mREIT catalysts/elements: 1) projected future MBS/funding worth actions; 2) projected future by-product valuations; and 3) projected near-term (as much as 1-year) dividend per share charges. This contains all current, present, and projected macroeconomic indicators and FOMC financial coverage.

mREIT Sector Suggestions as of three/15/2024:

As soon as once more utilizing Desk 1b above as a reference, I need to spotlight to readers what I/we’re conveying to subscribers with regards to sector suggestions as of three/15/2024 (final Friday’s shut).

As of three/15/2024, I/we had a STRONG BUY suggestion (notably undervalued) on the next mREIT shares analyzed above (in no explicit order): 1) MITT; 2) RC; and 3) GPMT. Simply know MITT and GPMT stay characterised as “speculative performs”.

As of three/15/2024, I/we had a BUY suggestion (undervalued) on the next mREIT shares analyzed above (in no explicit order): 1) CIM; 2) EFC; 3) NYMT; 4) RITM; 5) PMT; 6) BXMT; and 7) FBRT. Simply know CIM and NYMT stay characterised as “speculative performs”.

As of three/15/2024, I/we had a HOLD suggestion (appropriately valued) on the next mREIT shares analyzed above (in no explicit order): 1) ARR; 2) CHMI; 3) DX; 4) NLY; 5) TWO; 6) MFA; and seven) ACRE.

As of three/15/2024, I/we had a SELL suggestion (overvalued) on the next mREIT shares analyzed above (in no explicit order): 1) AGNC; 2) IVR; and three) ORC.

So, as of three/15/2024 I/we now have 3 mREITs rated as a STRONG BUY, 7 rated as a BUY, 7 rated as a HOLD, 3 rated as a SELL, and 0 rated as a STRONG SELL. Merely put, extra bullish when in comparison with the December – March 2023 and August – September 2023 however a bit much less bullish when in comparison with April – July 2023 and October – November 2023.

PART 2 of this text will cowl dividend metrics for the first quarter of 2024 and projections for the second quarter of 2024. Readers in search of my/our mREIT dividend projections for the primary quarter of 2024 can look in final quarter’s article (hyperlink offered close to the start of this text).

My Private RITM Previous + Present Inventory Disclosures:

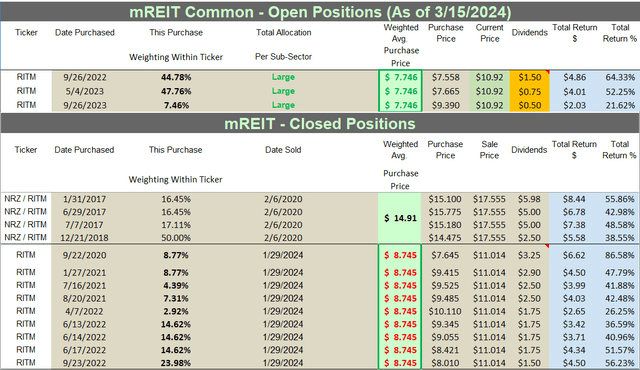

The next are my RITM (previously NRZ) previous and present inventory disclosures and complete returns since I’ve been writing on Searching for Alpha (since 2013):

Desk 8 – RITM Previous + Present Inventory Disclosures/Returns

The REIT Discussion board

Remaining Observe: All trades/investments I’ve carried out over the previous 7+ years have been disclosed to readers in “actual time” (that day on the newest) through both the StockTalks characteristic of Searching for Alpha or, extra lately, the “reside chat” characteristic of our Investing Group (which can’t be modified/altered). By means of these assets, readers can search for all my prior disclosures (buys/sells) relating to all firms I cowl right here at Searching for Alpha (see my profile web page for an inventory of all shares lined). By means of StockTalk disclosures and/or the reside chat characteristic of our Investing Group, on the finish of February 2024 I had an unrealized/realized achieve “success price” of 88.9% and a complete return (together with dividends acquired) success price of 95.8% out of 72 complete previous and current mREIT and enterprise growth firm (“BDC”)positions (up to date month-to-month; a number of purchases/gross sales in a single inventory rely as one general place till totally closed out). I encourage different Searching for Alpha contributors to offer actual time purchase and promote updates for his or her readers/subscribers which might in the end result in better transparency/credibility. Starting in January 2020, I transitioned all my real-time buy and sale disclosures solely to members of our Investing Group. All relevant public articles will nonetheless have my “foremost ticker” buy and sale disclosures (simply not real-time alerts).

Merely put, a contributor’s/crew’s suggestion observe file ought to “rely for one thing” and will at all times be thought-about with regards to credibility/profitable investing.

Understanding My/Our Valuation Methodology Relating to mREIT Frequent and BDC Shares:

The fundamental “premise” round my/our suggestions within the mREIT widespread and BDC sectors is worth. Relating to operational efficiency over the long run, there are above common, common, and beneath common mREIT and BDC shares. That mentioned, better-performing mREIT and BDC friends may be costly to personal, in addition to being low-cost. Simply because a well-performing inventory outperforms the corporate’s sector friends over the long run, this doesn’t imply this inventory ought to be owned at any worth. As with every inventory, there’s a worth vary the place the valuation is affordable, a worth the place the valuation is dear, and a worth the place the valuation is suitable. The identical holds true with all mREIT widespread and BDC friends. As such, relating to my/our investing methodology, every mREIT widespread and BDC peer has their very own distinctive BUY, SELL, or HOLD suggestion vary (relative to estimated CURRENT BV/NAV). The higher-performing mREITs and BDCs usually have a suggestion vary at a premium to BV/NAV (various percentages primarily based on general outperformance) and vice versa with the common/underperforming mREITs and BDCs (usually at a reduction to estimated CURRENT BV/NAV).

Every firm’s suggestion vary is “pegged” to estimated CURRENT BV/NAV as a result of this manner subscribers/readers can observe when every mREIT and BDC peer strikes throughout the assigned suggestion ranges (day by day if desired). That mentioned, the underlying reasoning why I/we place every mREIT and BDC suggestion vary at a unique premium or (low cost) to estimated CURRENT BV/NAV is predicated on roughly 15-20 catalysts which embrace each macroeconomic catalysts/elements and company-specific catalysts/elements (each constructive and detrimental). This investing technique is not for all market contributors. As an illustration, unlikely a “good match” for terribly passive buyers. For instance, buyers holding a place in a specific inventory, regardless of the worth, for say a interval of 5+ years. Nevertheless, as proven all through my articles written right here at Searching for Alpha since 2013, within the overwhelming majority of situations I’ve been in a position to improve my private complete returns and/or reduce my private complete losses from particularly implementing this explicit investing valuation methodology. I hope this offers some added readability/understanding for brand new subscribers/readers relating to my valuation methodology utilized within the mREIT widespread and BDC sectors.

Every investor’s BUY, SELL, or HOLD resolution is predicated on one’s danger tolerance, time horizon, and dividend revenue targets. My private suggestion won’t match every reader’s present investing technique. The factual data offered inside this text is meant to assist help readers with regards to investing methods/selections. Please disregard any minor “beauty” typos if/when relevant.

{kind=link}