dszc

Earnings of Southside Bancshares, Inc. (NASDAQ:SBSI) will probably enhance solely barely this 12 months. Subdued mortgage development will probably help earnings. In the meantime, the online curiosity margin will probably stay unchanged. Total, I am anticipating Southside Bancshares to report earnings of $2.88 per share for 2024, up 2.1% year-over-year. The year-end goal value suggests a mid-single-digit upside from the present market value. Moreover, the corporate is providing a beautiful dividend yield. Primarily based on the full anticipated return, I am upgrading Southside Bancshares to a purchase score.

Mortgage Development to Stabilize After Current Deceleration

The expansion of Southside Bancshares’ mortgage portfolio declined within the first quarter of 2024 after a outstanding efficiency within the final three quarters of 2023. Loans grew by 1.2% in the course of the first quarter, or 4.6% annualized, which was beneath final 12 months’s price of 9.0% and the five-year compounded annual development price of 6.4%.

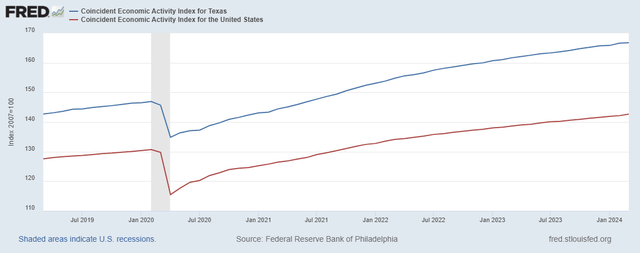

Going ahead, I feel mortgage development is unlikely to worsen any additional. Southside Bancshares operates in Texas’ main markets, specifically East Texas, Dallas-Fort Value, Southeast Texas, Austin, and Houston. Additional, a majority of Southsides’ loans are below the Business Actual Property (“CRE”) class. In consequence, the state of enterprise exercise in Texas is a crucial indicator of mortgage development within the close to time period. As proven beneath, Texas’ financial exercise coincident index seems to be higher in comparison with the nationwide common (discover how the hole between the 2 trendlines is widening.)

The Federal Reserve Financial institution of Philadelphia

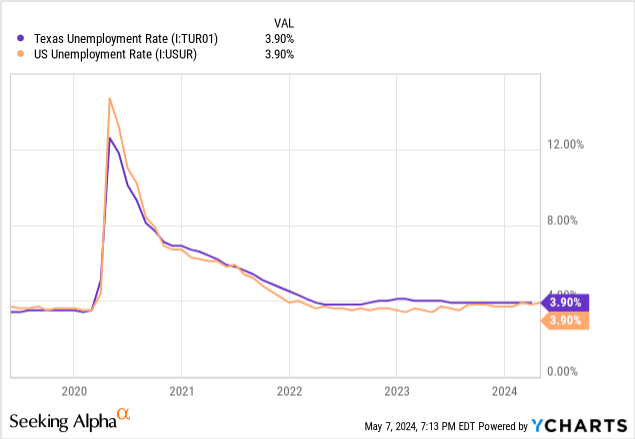

The index above incorporates the unemployment price, together with three different financial indicators (particulars). Trying on the unemployment price alone gives the look that Texas’ economic system is not significantly better than the nationwide common.

Contemplating the present financial setting, I feel mortgage development can proceed to stay at a passable degree within the close to time period. I am anticipating the mortgage portfolio to proceed to develop on the first quarter’s degree of 1.2% for the rest of the 12 months, resulting in full-year mortgage development of 4.8%. The next desk reveals my steadiness sheet estimates.

| Monetary Place | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E |

| Web Loans | 3,543 | 3,609 | 3,610 | 4,111 | 4,482 | 4,699 |

| Development of Web Loans | 7.8% | 1.8% | 0.0% | 13.9% | 9.0% | 4.8% |

| Different Incomes Belongings | 2,588 | 2,733 | 2,994 | 2,720 | 3,074 | 3,170 |

| Deposits | 4,703 | 4,932 | 5,722 | 6,198 | 6,550 | 6,784 |

| Borrowings and Sub-Debt | 1,160 | 1,113 | 543 | 533 | 877 | 938 |

| Frequent fairness | 805 | 875 | 912 | 746 | 773 | 920 |

| E book Worth Per Share ($) | 23.7 | 26.3 | 27.9 | 23.1 | 25.1 | 30.4 |

| Tangible BVPS ($) | 17.4 | 20.0 | 21.5 | 16.8 | 18.5 | 23.6 |

| Supply: SEC Filings, Writer’s Estimates(In USD million except in any other case specified) | ||||||

Margin More likely to Stabilize

Southside Bancshares’ internet curiosity margin continued to say no for the fifth consecutive quarter in the course of the first quarter of the 12 months. The margin shrank by 13 foundation factors within the first quarter of 2024 after declining by a cumulative 41 foundation factors by means of 2023.

A lot of the margin stress was attributable to the steadily worsening deposit combine. Non-interest-bearing deposits shrank to twenty.8% of complete deposits by the tip of March 2024 from 21.2% on the finish of December 2023 and 26.4% on the finish of March 2023. Rate of interest hikes inspired deposit migration as depositors have been tempted by increased charges. Deposit combine deterioration is more likely to taper off as soon as rates of interest begin declining, probably within the second half of this 12 months. In consequence, the stress on the margin from deposit migration will probably finish quickly.

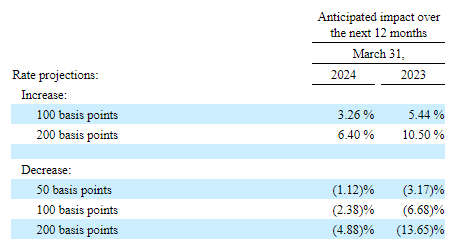

Then again, the re-pricing of property and liabilities after price cuts later this 12 months will damage the margin. The outcomes of the administration’s rate-sensitivity evaluation given within the 10-Q submitting present {that a} 50-basis factors price lower might scale back the online curiosity earnings by 1.12% over twelve months.

1Q 2024 10-Q Submitting

Contemplating these conflicting components, I am anticipating the online curiosity margin to stay unchanged from the primary quarter’s degree of two.86% for the rest of the 12 months.

Expense Management Measures to Help Earnings

The administration talked about within the convention name, “Because of the associated fee containment initiatives, we count on to comprehend roughly $400,000 of financial savings within the second quarter and $700,000 to $800,000 within the third and fourth quarters of the 12 months.” Whereas these initiatives will constrain working bills, inflation will push up the working bills. The sharp disinflation seen final 12 months is now flattening, and inflation continues to be fairly excessive. Contemplating the consequences of inflation and cost-control measures, I am anticipating the non-interest bills to develop at a below-average price of 0.05% in every of the three remaining quarters of 2024.

Contemplating my steadiness sheet, internet curiosity margin, and non-interest expense outlook, I am estimating earnings of $2.88 per share for 2024. To reach at my earnings estimate, I’ve additionally assumed that non-interest earnings will stay secure on the first quarter’s degree and that the supply expense will return to the 2022 degree after an uncommon motion within the third quarter of final 12 months.

The next desk reveals my earnings assertion estimates.

| Earnings Assertion | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E |

| Web curiosity earnings | 170 | 187 | 190 | 212 | 215 | 217 |

| Provision for mortgage losses | 5 | 20 | (17) | 3 | 9 | 3 |

| Non-interest earnings | 42 | 50 | 49 | 41 | 36 | 39 |

| Non-interest expense | 119 | 123 | 125 | 130 | 141 | 148 |

| Web earnings – Frequent Sh. | 75 | 82 | 113 | 105 | 87 | 87 |

| EPS – Diluted ($) | 2.20 | 2.47 | 3.47 | 3.26 | 2.82 | 2.88 |

| Supply: SEC Filings, Writer’s Estimates(In USD million except in any other case specified) | ||||||

Dangers Are Manageable

Southside Bancshares’ threat degree is low. The credit score threat of its mortgage portfolio seems manageable with nonaccrual loans making up simply 0.17% of complete loans. Additional, the unrealized mark-to-market losses on the Out there-for-Sale securities portfolio totaled $51.6 million on the finish of March 2024, which is simply 7% of the full fairness ebook. Additional, uninsured and uncollateralized deposits have been simply 18.5% of complete deposits as of March 31, 2024, as talked about within the 10-Q Submitting.

Dividend Yield is Over 5%

Southside Bancshares is presently providing a really engaging dividend yield. The present quarterly dividend of $0.36 per share and the most recent market value recommend a dividend yield of 5.17%. The corporate additionally normally pays an annual particular dividend. Assuming the corporate maintains the particular dividend for this 12 months finally 12 months’s degree of $0.02 per share results in an all-inclusive dividend yield of 5.24%. The dividend seems secure due to the next two components:

- The quarterly and particular dividends mixed recommend a payout ratio of fifty.7% for 2024. That is fairly near the five-year common of 48.5%.

- Southside Bancshares is effectively capitalized, so there aren’t any threats of a dividend lower from regulatory necessities. The corporate reported a complete capital ratio of 15.92% for the tip of March 2024, which is comfortably increased than the minimal regulatory requirement of 10.50%.

Upgrading to a Purchase Score

I am utilizing the peer common price-to-tangible ebook (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Southside Bancshares. Friends are buying and selling at a median P/TB ratio of 1.27 and a median P/E ratio of 10.0, as proven beneath.

| SBSI | LBAI | BFC | FBMS | CTBI | BRKL | Peer Common | |

| P/E (“ttm”) | 10.2 | 9.9 | 10.7 | 10.0 | 10.0 | 9.6 | 10.0 |

| P/B (“ttm”) | 1.06 | 0.71 | 1.36 | 0.83 | 1.10 | 0.65 | 0.9 |

| P/TB (“ttm”) | 1.44 | 0.95 | 2.04 | 1.28 | 1.23 | 0.84 | 1.27 |

| Supply: Searching for Alpha | |||||||

Multiplying the common P/TB a number of with the forecast tangible ebook worth per share of $23.6 offers a goal value of $30.0 for the tip of 2024. This value goal implies a 7.7% upside from the Could 8 closing value. The next desk reveals the sensitivity of the goal value to the P/TB ratio.

| P/TB A number of | 1.07x | 1.17x | 1.27x | 1.37x | 1.47x |

| TBVPS – Dec 2024 ($) | 23.6 | 23.6 | 23.6 | 23.6 | 23.6 |

| Goal Value ($) | 25.3 | 27.6 | 30.0 | 32.3 | 34.7 |

| Market Value ($) | 27.9 | 27.9 | 27.9 | 27.9 | 27.9 |

| Upside/(Draw back) | (9.3)% | (0.8)% | 7.7% | 16.1% | 24.6% |

| Supply: Writer’s Estimates |

Multiplying the common P/E a number of with the forecast earnings per share of $2.88 offers a goal value of $28.9 for the tip of 2024. This value goal implies a 3.7% upside from the Could 8 closing value. The next desk reveals the sensitivity of the goal value to the P/E ratio.

| P/E A number of | 8.0x | 9.0x | 10.0x | 11.0x | 12.0x |

| EPS 2024 ($) | 2.88 | 2.88 | 2.88 | 2.88 | 2.88 |

| Goal Value ($) | 23.1 | 26.0 | 28.9 | 31.8 | 34.6 |

| Market Value ($) | 27.9 | 27.9 | 27.9 | 27.9 | 27.9 |

| Upside/(Draw back) | (17.0)% | (6.6)% | 3.7% | 14.0% | 24.4% |

| Supply: Writer’s Estimates |

Equally weighting the goal costs from the 2 valuation strategies offers a mixed goal value of $29.4, which suggests a 5.7% upside from the Could 8 market value. Including the ahead dividend yield offers a complete anticipated return of 10.9%.

In my final report on Southside Bancshares, which was issued again in July 2023, I adopted a maintain score with a December 2023 goal value of $26.8. Since then, the inventory value has plunged. Primarily based on the up to date complete anticipated return, I am upgrading Southside Bancshares to a Purchase Score.

{kind=link}