Nutthaseth Vanchaichana/iStock through Getty Pictures

The best way the primary quarter went, with transient and really shallow pullbacks, one would suppose that shares are partying like it’s 1995. Whereas it’s silly to extrapolate one quarter into an entire yr, 1995 involves thoughts, as that was the one delicate financial touchdown engineered by the Fed in latest U.S. historical past, because the Fed started chopping rates of interest after elevating them for a yr and the inventory market went dramatically larger.

The S&P 500 return in 1995? On a price-only foundation, +34.1%, or +37.1% with dividends reinvested. The speed chopping cycle that started in 1995 had three fee cuts, just about what the Fed has deliberate for 2024.

The S&P 500 (adjusted by the CPI) Since 1995

Graphs are for illustrative and dialogue functions solely. Please learn necessary disclosures on the finish of this commentary.

Whereas the final level on the chart represents the current stage of the S&P 500 Index, each level going backwards is inflated by the extent of the Shopper Worth Index (CPI). By that measure, the S&P 500 set its all-time excessive on the finish of 2021 at 5304, so if one had been to regulate for inflation, the current stage of the S&P 500 Index has not made an all-time excessive in actual phrases. If rates of interest had been to say no 1995 model, one may see fairly a bit additional appreciation for shares from right here.

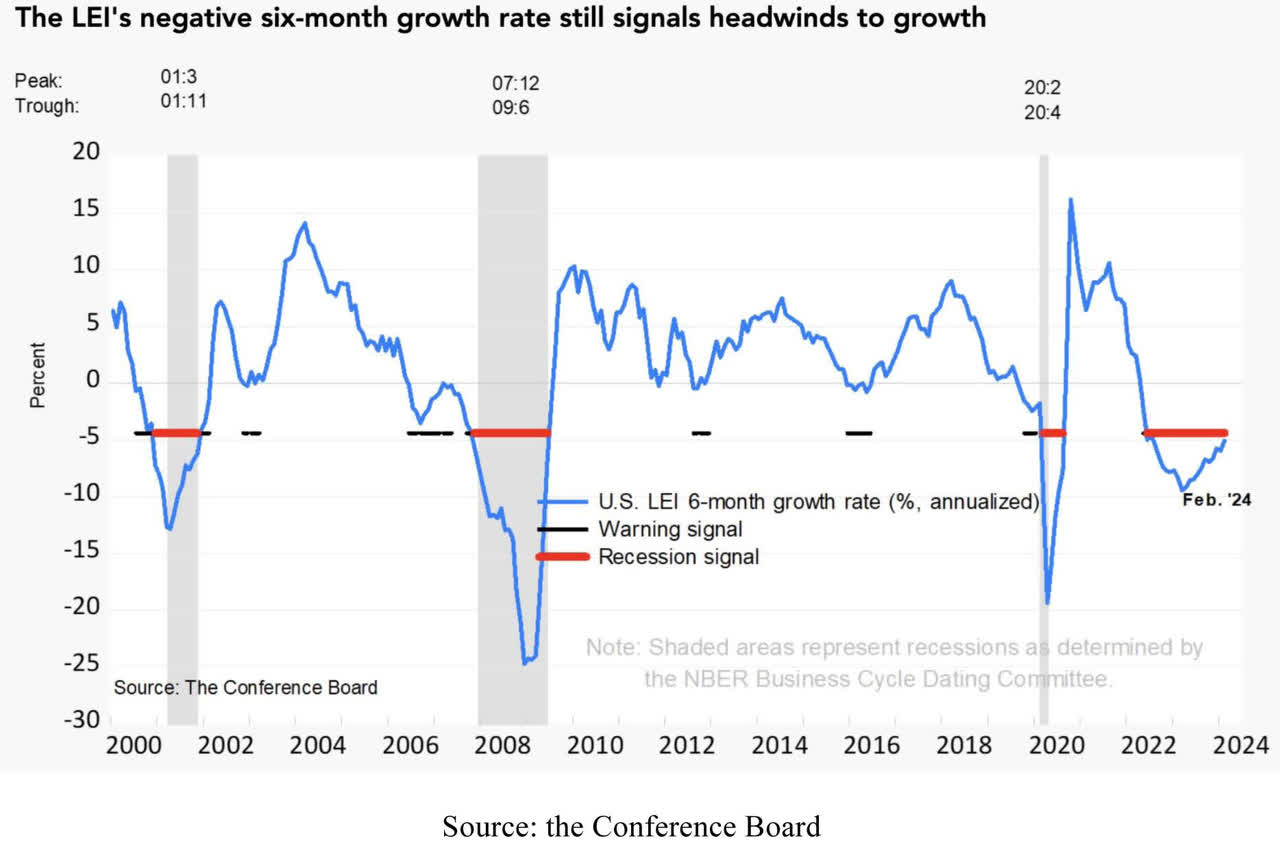

The Convention Board’s Index of Main Financial Indicators (LEI) has been forecasting a recession that by no means got here, for a very long time, however final month, it lastly turned constructive. The index continues to be adverse, however because it has risen from a depressed stage as a lot because it has, it has by no means in latest historical past turned down once more.

Graphs are for illustrative and dialogue functions solely. Please learn necessary disclosures on the finish of this commentary.

In reality, such an increase within the LEI is definitely forecasting the start of an financial enlargement. We might have headwinds to progress, however a full-blown recession is way tougher to see vs. the identical time final yr when most predicted a recession. Perhaps, simply perhaps, that is what an financial delicate touchdown seems to be like.

Authorities Debt is Relative – Even when Out of Management

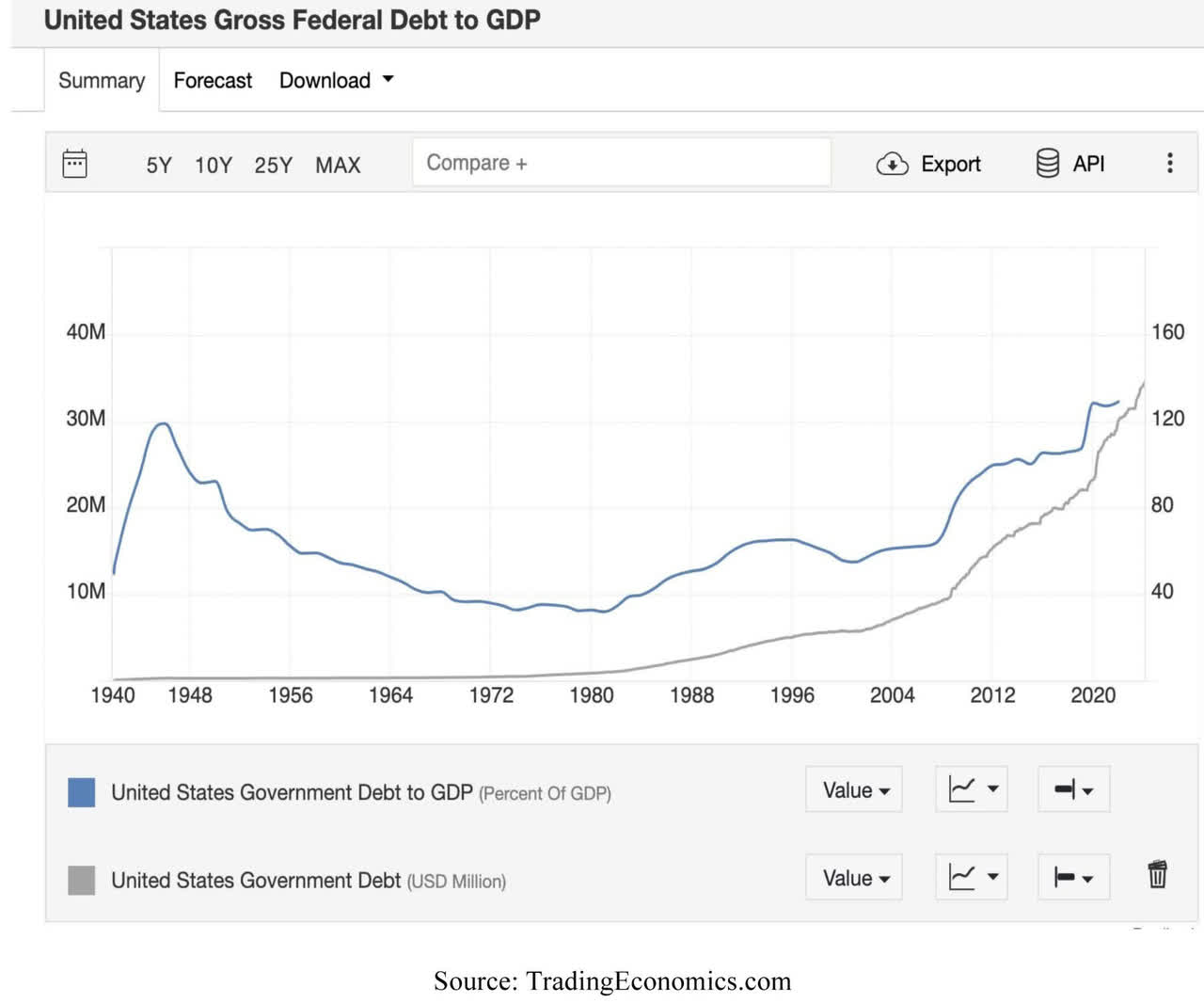

The current stage of U.S. authorities debt is about $34.5 trillion and going up by about $1 trillion each 90 days, with curiosity this yr reaching $1.6 trillion. The state of affairs clearly is uncontrolled and ought to be addressed. The issue, or some would possibly say the answer, is that we’ve been there earlier than.

Graphs are for illustrative and dialogue functions solely. Please learn necessary disclosures on the finish of this commentary.

The federal government debt-to-GDP ratio is above 130% at current. It was round 120% of GDP proper after World Battle II, after which balanced budgets introduced it again down, however this time somebody must rein in deficit spending in an election yr, and that’s exhausting to think about. If a brand new authorities is available in after the elections, I feel taking management of the debt state of affairs ought to be a prime precedence, even when it creates a recession.

What inflation did within the final three years is to lower the true worth of the substantial current money owed. The U.S. did inflate away a lot of its WW2 money owed. Whereas inflation got here down slowly over time again then, it positive seems to be just like the federal authorities can also be inflating away a few of its COVID-era money owed proper now.

There’s nonetheless time to handle the debt downside, however not as a lot as most politicians suppose, as including new debt on the current trajectory will certainly create one other kind of disaster in not more than 5 years.

All content material above represents the opinion of Ivan Martchev of Navellier & Associates, Inc.

Disclaimer: Please click on right here for necessary disclosures situated within the “About” part of the Navellier & Associates profile that accompany this text.

Disclosure: *Navellier might maintain securities in a number of funding methods supplied to its purchasers.

Authentic Publish

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.

{kind=link}