Andrii Dodonov

Funding thesis

Sumitomo Mitsui Monetary Group (NYSE:SMFG) has confronted important headwinds within the final 12 months with Russian publicity and market manipulation at its funding banking arm Nikko Securities. Nonetheless, with its core enterprise performing in a steady method, we imagine the potential dividend yield of 6.2% is engaging. We reiterate our purchase ranking on the shares.

Fast primer

Sumitomo Mitsui Monetary Group is a Japanese business and retail financial institution with a primarily conservative home focus. Its ‘megabank’ friends are Mitsubishi UFJ Monetary Group (MUFG) and Mizuho Monetary Group (MFG). Its funding banking division known as SMBC Nikko Securities.

On September twenty eighth, 2022 the Japanese FSA issued its fourth administrative motion towards SMBC Nikko Securities, following the Securities and Trade Surveillance Fee’s announcement of its suggestion for administrative motion towards the corporate. The FSA is contemplating a partial enterprise suspension order and can be contemplating administrative motion towards the mother or father firm, Sumitomo Mitsui Monetary Group. Adverse points cited embrace a “sales-first company tradition,” and “little consciousness of authorized compliance”.

The watchdog criticized the corporate for “undermining the equity of the market”, and has filed felony costs towards SMBC Nikko Securities for allegedly manipulating the inventory costs of Koito Manufacturing (OTCPK:KOTMY), Mos Meals Service (8153), and different firms in reference to block provide buying and selling. The Tokyo District Public Prosecutors Workplace has charged the corporate’s former vice chairman and different executives with violating the Monetary Devices and Trade Legislation (market manipulation) by illegally shopping for shares.

We need to replace our view from our purchase ranking from August 2021, which was primarily based on expectations of enhancing shareholder returns given SMFG’s well-capitalized steadiness sheet.

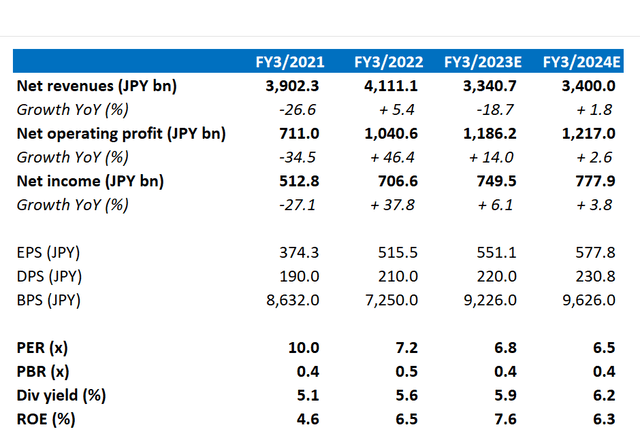

Key financials together with consensus estimates

Key financials together with consensus estimates (Refinitiv, firm)

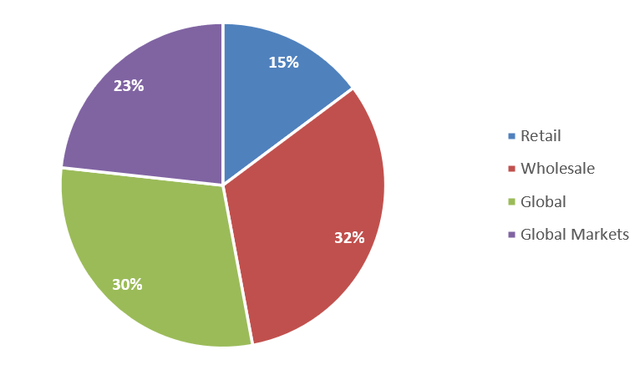

Internet enterprise revenue cut up per enterprise unit (FY3/2022)

Internet enterprise revenue cut up per enterprise unit (FY3/2022) (Firm)

Our goals

We need to replace our view from our purchase ranking from August 2021, which was primarily based on expectations of enhancing shareholder returns given SMFG’s well-capitalized steadiness sheet. The shares have corrected 20% – is it time so as to add or to promote?

The image (ignoring Nikko Securities)

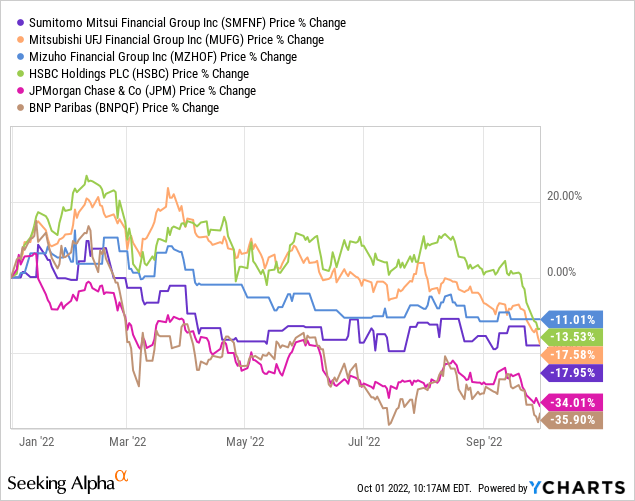

Japanese banks have outperformed their international friends YTD in CY2022, the first causes being 1) the restricted contribution from international market actions (equivalent to funding banking) 2) their comparatively over-capitalized steadiness sheets and three) conservative administration that resulted in predictable credit score prices. In essence, Japanese banks are steady and undynamic companies, and even when beneath a cloud with unfavorable reputational points as per SMFG, the shares don’t dramatically underperform their friends (chart beneath shares relative efficiency YTD).

SMFG’s Q1 FY3/2023 outcomes highlighted a surprisingly strong efficiency albeit from a low base YoY, with abnormal revenue development of 64% YoY (slide 5). Progress was pushed by the next elements.

Retail operations noticed probably the most development in capturing cost commissions, pushed by Japan’s belated however materializing cashless marketplace for each buying and issuer companies. As shoppers and retailers undertake credit score and debit playing cards, e-money, and QR code settlement, this has develop into a brand new earnings driver in what has been a predominantly cash-driven market.

Wholesale operations noticed steading enhancements YoY throughout the board, however with the fluctuations in FX markets, cash switch charges have been notably robust. The mortgage e book grew 14% YoY as urge for food for credit score recovered, and asset high quality noticed continued enhancements with falling credit score prices and non-performing loans falling to 0.92% QoQ from 1.08% in FY3/2022.

SMFG took a JPY100bn/USD0.7bn hit on Russian publicity in FY3/2022, and we take the view that there will likely be some extra losses to soak up throughout FY3/2023. Nonetheless, firm disclosure states that further impairment for the plane leasing enterprise is USD0.46m, and additional credit score prices, in addition to expropriation bills for the native subsidiary, might happen; we imagine these will likely be whole considerably decrease YoY, with some upside if insurance coverage claims come via for the aviation enterprise. With expectations of a gradual restoration, SMFG has elevated its publicity in aviation with the acquisition of Goshawk, which is predicted to contribute accretive earnings for the medium to long run.

Current buying and selling reveals that SMFG is working on a steady and sustainable foundation, though International Markets is visibly weak which contributed 25% of whole internet enterprise revenue in FY3/2022 – we have a look at this subsequent.

Implications over Nikko Securities going forwards

After main insider buying and selling circumstances, Japan’s regulator is making an instance of Nikko Securities, SMFG’s brokerage arm. On a sensible foundation, that is unfavorable for the enterprise as it would disallow participation in profitable funding banking actions equivalent to IPOs and different fairness choices as key e book runners, in addition to underwriting company bond issuances. Consequently, Nikko noticed internet working revenues fall almost 40% YoY in Q1 FY3/2023.

Regardless of this unfavorable growth, from a share value perspective, we really feel that this episode has been priced in. There will likely be continued scrutiny by the regulator, however we count on SMFG will reply in an acceptable method by ensuring it turns into compliant and displaying enhancements and modifications inside its group. On a optimistic be aware, international markets are usually not the important thing earnings contributor on the financial institution, versus friends equivalent to Mizuho and different funding banks equivalent to Nomura (NMR) and Daiwa (OTCPK:DSEEY).

Except additional unfavorable points are uncovered on the financial institution, we imagine that Nikko Securities poses a comparatively low threat to the shares now. In something, this funding banking arm is about to develop into extra conservative than earlier than. A scarcity of dynamism could also be seen as unfavorable, however contemplating Nikko Securities is successfully a comparatively new operation arrange in 2009 (as Citigroup purchased the unique high-quality brokerage, and SMFG broke ranks with a partnership with Daiwa), its historical past is comparatively brief and was performing in an improper method with the intention to meet up with its established home friends – the danger profile is about to fall which is a optimistic.

Valuation

On consensus forecasts (see Key financials desk above), the potential dividend yield is 6.2%, on an ROE of 6.3%. We imagine that the unfavorable occasions that influenced share value efficiency within the final 12 months are now not a long-term concern. On this foundation, we imagine the dividend yield on provide is engaging.

With a comparatively strong begin to FY3/2023, we imagine the dividend steering of JPY220 is just not beneath menace. The share buyback program of JPY100bn/USD0.7bn that was deliberate for FY3/2022 is but to begin – we count on this in H1 FY3/2024 as soon as macro situations start to stabilize.

Key dangers

Upside threat comes from saying an accelerated share buyback program, re-starting the preliminary program from FY3/2022 in addition to a further one. If the corporate maintains its coverage of a 40% dividend payout ratio, any upside to FY3/2023 earnings steering might imply a notable dividend hike YoY.

Draw back threat comes from Russia – though we imagine the losses booked in FY3/2022 are adequate, there may be an overhang associated to additional credit score prices and delayed timing over insurance coverage compensation for the aviation enterprise. Any important enhance in credit score prices from its abroad mortgage e book might pose issues for its core business banking enterprise.

Conclusion

SMFG has confronted important headwinds within the final 12 months with Russian publicity and market manipulation at its funding banking arm Nikko Securities. We imagine these points have already been priced in, and on a long-term foundation don’t pose a significant threat to the financial institution. With a steady dividend yield of 6.2% on provide, we imagine the shares stay a purchase.

{kind=link}