PonyWang

We’re bullish on the Taiwanese Semiconductor Manufacturing Firm (NYSE:TSM). We love companies with a singular focus. In TSM’s case, it’s a pure-play foundry enterprise. TSM is taken into account the producer of selection for main semiconductor firms worldwide. We don’t consider the geopolitical tensions change that TSMC is the best-positioned chipmaker within the semiconductor business, with a roughly 53% market share of the worldwide foundry market. TSMC controls the chips-to-order foundry marketplace for among the world’s most vital semiconductor companies- Nvidia (NVDA), Superior Micro Gadgets (AMD), Broadcom (AVGO), and Apple (AAPL). Even underneath the present macroeconomic atmosphere, we consider TSMC is well-positioned to develop for a number of years. With TSMC opening fabs in Arizona, the corporate is taking steps to de-risk from geopolitical tensions in Asia. We consider TSMC is affordable at present ranges and suggest buyers purchase the inventory.

Nonetheless the face of pure-play foundry

World digitalization is underway now greater than ever, which interprets to extra demand for semiconductor chips, particularly these made by TSMC. TSMC is the world’s largest contract producer of semiconductor chips required to energy our telephones, automobiles, and fridges, amongst all different points of each day life. Therefore, we don’t see demand for the chip-maker weakening meaningfully. Nonetheless, TSMC shouldn’t be resistant to semiconductor cycles. TSMC reported a 47.9% Y/Y improve in revenues in its newest quarter, regardless of the semiconductor business slowdown.

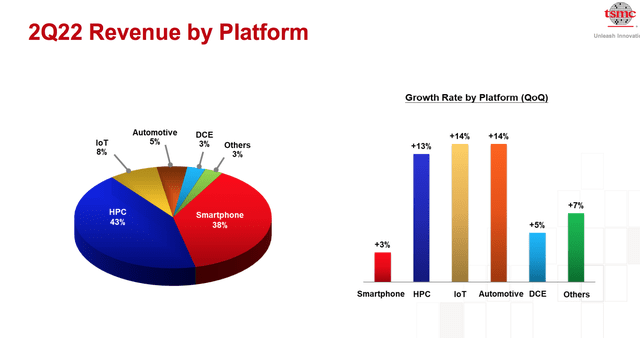

Weakening client demand has been the central theme for 2022, and TSMC shouldn’t be resistant to market volatility. TSMC is particularly uncovered to the decline in PC and smartphone demand. The next graph from the corporate’s 3Q22 earnings outlines TSMC’s income by platform.

TSM

World PC shipments have declined 19.5% over the previous 12 months, and PCs are forecasted to say no once more in 2022. Smartphone shipments are additionally forecasted to drop by 6.5% in 2022.

Regardless of present macroeconomic headwinds, TSMC reported income and gross margins forward of estimates final week, main the inventory to rally after its outcomes final week. TSMC inventory remains to be down round 37% YTD. We attribute TSMC inventory fall to weakening client demand throughout the business at giant. We consider the inventory pullback creates a horny entry level to take a position on the planet’s main chipmaker.

Elevating ASP because it makes smaller and smaller chips

TSMC has an enormous benefit with its course of expertise, because it permits the corporate to fabricate chips cost-efficiently with the best transistor density with prime quality/yield. With shrinking transistor sizes, the prices of producing superior course of nodes are rising. 3nm course of node chips are extra complicated to fabricate, and TSMC is elevating the costs for these newer chips. TSMC elevating ASP for superior course of nodes will profit the corporate sooner or later. We count on the upper ASP will make the corporate extra resilient to market downturns because it gives extra cushion to climate storms. AAPL has already contracted TSMC to supply the 3nm chip tech subsequent 12 months. We’re optimistic that TSMC will more and more achieve shares on superior course of nodes going ahead.

Regional focus is a matter for now

Greater than half the worldwide made-to-order chip foundry capability is concentrated in Taiwan, which is more and more turning into a problem because the “tech wars” between the US and China unfold. Geopolitical issues about China doubtlessly invading the Island are intensifying, particularly, after US Home Speaker Nancy Pelosi visited Taiwan this August. Regional focus is a matter, however we consider it’s only a problem for now.

We consider the regional focus is easing as TSMC cooperates with the US’s CHIPS Act and plans to carry chip-making to US soil. TSMC has introduced that its foundry enterprise will increase and manufacture 5nm chips in Arizona. The corporate has already invested $12B in constructing its Arizona-based fabs. We consider TSMC is taking the required steps to dilute its regional focus going ahead.

Too helpful to invade: international silicon protect

Media and monetary pundits are hyping issues over the attainable Chinese language invasion of Taiwan with numerous “what if China invades?” speak. We consider TSMC is simply too helpful to China for it to invade the Island anytime quickly. China nonetheless consumes the majority of the worldwide chip provide, with 36% estimated to come back from Taiwan in 2021. We consider Taiwan’s chip-making worth gives it with a world silicon protect that may deter any invasion within the intermediate time period.

Valuation

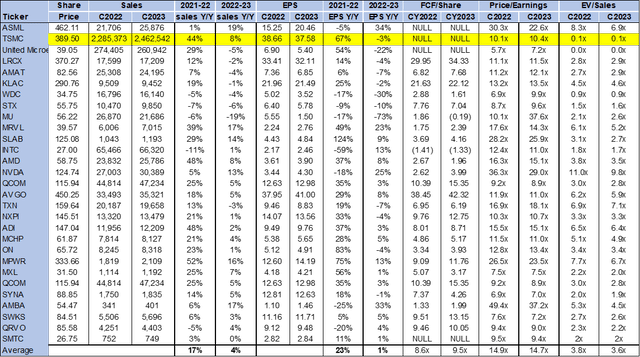

TSMC inventory is comparatively low cost, buying and selling at 10.4x C2023 EPS of $37.58 on the P/E foundation in comparison with the group common of 14.7x. The inventory is buying and selling at 0.1x EV/C2023 gross sales versus the peer group common of three.6x. The next chart illustrates the semiconductor peer group valuation.

Refinitiv

Phrase on Wall Avenue

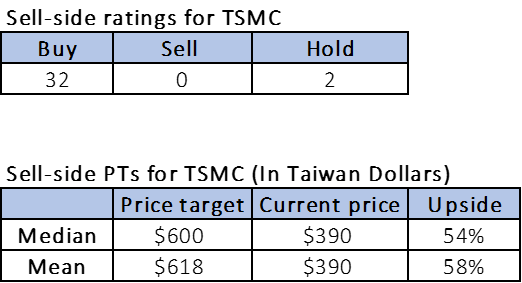

Wall Avenue is overwhelmingly buy-rated on the inventory, and we agree with that sentiment. Of the 34 analysts masking the inventory, 32 are buy-rated, and the remaining are hold-rated. TSMC is buying and selling at round $390. The median value goal is $600, and the imply value goal is $618, with a possible upside of 54-58%. The next chart signifies TSMC sell-side rankings and value targets:

Refinitiv

What to do with the inventory

The present macroeconomic and demand atmosphere has triggered the inventory to drop, however we consider the chip-making business remains to be rising. For F3Q22, TSMC reported income development and beat estimates, and we don’t count on the corporate’s development to decelerate because it stays the best-positioned foundry participant with a stable buyer base. We consider the inventory pullback and the depressed valuation create a horny entry level to put money into the foundry business, and suggest buyers purchase at present ranges.

{kind=link}