By ROSEMARIE DAY and DAVID W. JOHNSON,

The Reasonably priced Care Act (ACA) survived its third problem on the Supreme Court docket on June 18, 2021, by a 7-2 vote, signaling that Obamacare is right here to remain. With a divided Congress and a Biden administration challenged by a number of urgencies, there’s little hope for nationwide laws to deal with healthcare’s entry, price, and high quality deficiencies comprehensively.

Regardless of this lack of dramatic progress or sweeping change on the federal stage, reformers needn’t lose hope. Quietly, state-based marketplaces are making medical health insurance provision extra accessible, inexpensive and efficient.

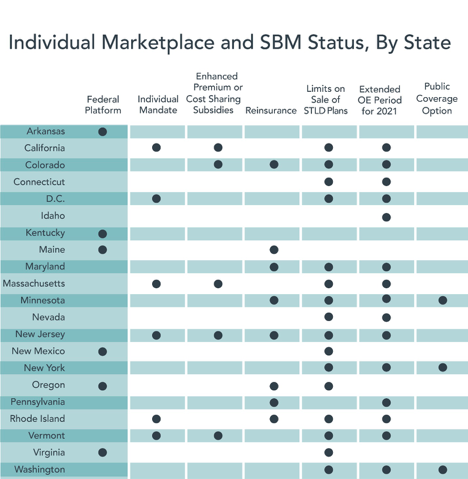

A Biden Administration’s govt order signed in January 2021, reopened the federal medical health insurance market to people searching for to buy or modify medical health insurance insurance policies. The fifteen state-based marketplaces (SBMs) adopted go well with by enacting their very own variations of this particular enrollment interval.

The Administration’s $1.9 trillion American Rescue Plan, enacted on March 11, 2021, features a slender however highly effective provision that briefly grants premium subsidies to higher-income Individuals and reduces premium prices for lower-income Individuals. The “Construct Again Higher Act” presently shifting by the Home of Representatives would make these subsidies everlasting. It might additionally present funding for extra experimentation with state-based medical health insurance affordability applications.

These new insurance policies align with measures undertaken by many SBMs in the course of the previous eight years to enhance the standard, affordability, and marketability of their medical health insurance choices. On this decentralized, real-world method, SBMs have operated as experimental coverage laboratories to evaluate programming modifications for stabilizing native markets, increasing shopper selection, rising entry to very important healthcare companies, and reducing premiums.

Profitable SBM improvements have demonstrated that insurance coverage marketplaces can adapt and thrive by responding to shopper preferences. By increasing to extra states, adopting confirmed cures, and extra successfully overseeing plan sponsors, SBMs can present much more Individuals with entry to the inexpensive well being and wellness companies they want.

THE EVOLUTION OF STATE-BASED MARKETPLACES

Enacted in 2010, the ACA launched pointers and supplied start-up funding for SBMs. The laws’s goal was to create inexpensive medical health insurance choices that Individuals missing medical health insurance protection may buy on market-based exchanges.

Impressed by Massachusetts healthcare reform (aka “Romneycare”), the framework constructed on non-ACA buying cooperatives providing “small group” medical health insurance plans. The brand new marketplaces enabled particular person customers to buy ACA-compliant medical health insurance protection on-line. The ACA additionally supplied income-based subsidies for certified enrollees.

The ACA’s designers believed that almost all states would develop their very own marketplaces. They established HealthCare.gov, a federally operated various, to supply entry to ACA plans in states that selected to not create SBMs.

Political resistance impeded the widespread adoption of SBMs on the outset. But, SBMs haven’t solely thrived within the years since they’re now poised to broaden. Kentucky, Maine, and New Mexico are launching their very own state-run marketplaces this fall for operation in Plan 12 months 2022. Others, together with Virginia, will doubtless observe.

Supply knowledge: Kaiser Household Basis https://www.kff.org/health-reform/state-indicator/state-health-insurance-marketplace-types/?activeTab=map¤tTimeframe=0&selectedDistributions=marketplace-type&sortModel=%7Bpercent22colIdpercent22:%22Locationpercent22,%22sortpercent22:%22ascpercent22percent7D

SBMs function as marketplaces for insurers to compete in providing plans that meet ACA-regulated requirements. SBMs additionally promote enrollment, pool danger to decrease premiums, and facilitate comparability procuring.

A CRITICAL SAFETY NET

Together with HealthCare.gov, 12 million customers have enrolled in market-based plans for the calendar 12 months 2021, a rise of 600,000 from 2020. Over 3.8 million of the 12 million enrolled by SBMs. The overwhelming majority of enrollees (together with 88% of the customers enrolled by HealthCare.gov) obtain some monetary help within the type of subsidies.

Regardless of the elevated enrollment, greater than 30 million Individuals stay uninsured and 43.4% of the inhabitants has insufficient medical health insurance protection. The variety of uninsured individuals in America declined considerably with the implementation of the ACA in 2014, then started to rise in 2017 because the Trump Administration decreased assist for enrollment.

The pandemic-related financial shutdown appeared prone to balloon the ranks of the uninsured. As a substitute, employer-based protection largely held and lots of who discovered themselves all of a sudden uninsured secured protection by Medicaid or market well being plans.

The extension of the open enrollment interval and the improved subsidies have facilitated enrollment in SBMs and HealthCare.gov this 12 months. For an estimated a million individuals, market well being plans supplied a vital security web.

CONTINUED GROWTH & IMPROVEMENT

Regardless of the charged political debate for the reason that ACA’s passage, SBMs have proven nice promise and resilience. Many SBMs have adopted focused options to make well being plan premiums extra enticing and inexpensive. Some have enabled customers to buy and evaluate plans extra simply. Others have included reinsurance, enhanced subsidies, and/or particular person mandates that strengthen the chance pool and assist to cut back costs.

Completely different approaches amongst states can result in drastic variations within the affordability and attractiveness of well being plan choices. Minnesota’s resolution to supply reinsurance to insurers with well being plans on its SBM lowered its 2021 month-to-month benchmark fee to $292. Throughout the state line in Wisconsin, the month-to-month benchmark fee jumped to $782. The 2021 nationwide common benchmark premium is $443 monthly.

Analysts, directors, and policymakers are finding out these totally different approaches to higher perceive the elements influencing the elasticity of demand in state and federal marketplaces. The outcomes might be hanging.

One research confirmed that the existence of particular person mandates in state-based marketplaces will increase the chance that people will buy medical health insurance insurance policies, no matter monetary penalties. Different research affirm that particular person tolerance for larger premiums will increase with a higher perceived want for medical health insurance, as happens with elements comparable to poor well being and older age. Such priorities enhance demand for medical health insurance and scale back value elasticity.

That mentioned, a standardized menu of inexpensive choices will increase shopper sensitivity to cost. States can undertake an evidence-based strategy by utilizing this sort of information to tweak program choices and make them extra enticing to market customers.

SBMs monitor one another’s methods carefully, typically adopting improvements applicable to native wants. Through the use of an evidence-based strategy, they will make their choices even stronger. Progress can even stimulate curiosity in different states for creating their very own marketplaces. As famous above, SBMs’ collective success has already influenced a number of historically crimson and purple states, together with Kentucky, Maine, New Mexico, and Virginia, that are actually implementing their very own SBMs.

With political headwinds now turning into tailwinds, SBMs are discovering it simpler to enact modest however sensible structural enhancements that may make their marketplaces much more sturdy and enticing. Development will proceed as extra product choices come to SBMs, customers acquire extra selections, value-driven transactions enhance, well being outcomes enhance and system-wide prices lower.

CONCLUSION: LOCAL SOLUTIONS ADVANCING MEANINGFUL REFORM

The ACA offers states the flexibleness to implement SBMs and encourage personal sector participation. The federal authorities is liable for establishing protection requirements, financing subsidies, and working the HealthCare.gov platform. However it faces some challenges on the subject of innovating.

Against this, states might be nimble. They will tailor program choices to fulfill market calls for and dynamics. Components influencing program design may additionally embrace the state’s city/rural combine, the scale of its employer base, the payer combine, social determinants of well being, demographics, and cultural attributes. This means to accommodate market preferences and different elements validates the federalist strategy that the ACA takes in granting SBM program design to the states.

This flexibility avoids the “one-size-fits-all” strategy included inside the federally run market. By tailoring their SBMs to native circumstances, the states have develop into very important engines of experimentation and innovation for advancing the general effectiveness of the nation’s healthcare marketplaces.

With enhanced program design and growth to extra states, together with assist from the Construct Again Higher Act, SBMs are well-positioned to function a catalyst for significant healthcare reform. Not all progress is revolutionary. As SBMs have demonstrated, evolutionary enhancements in profit design, enrollee engagement, danger administration, and outreach allow hundreds of thousands of American customers to realize inexpensive entry to high-quality care.

For added element, please see a abstract of those and lots of different state actions to assist entry to medical health insurance protection from the Commonwealth Fund: https://www.commonwealthfund.org/publications/maps-and-interactives/2021/sep/what-your-state-doing-affect-access-adequate-health?redirect_source=/publications/maps-and-interactives/2021/mar/what-your-state-doing-affect-access-adequate-health

Rosemarie Day is the founder and CEO of Day Well being Methods (www.dayhealthstrategies.com), a consulting agency devoted to remodeling the US healthcare system.

David Johnson is the CEO of 4sight Well being, a thought management and advisory firm working on the intersection of technique, economics, innovation, and capital formation.

Sources:

1 Andrews, M. (2021, February 15). As Biden Reopens ACA ENROLLMENT, are you eligible to enroll or change HEALTH PLANS? NPR. https://www.npr.org/sections/health-shots/2021/02/15/967366282/as-biden-reopens-aca-enrollment-are-you-eligible-to-sign-up-or-switch-health-pla.

2 Kliff, S. (2021, January 16). One sentence In Biden stimulus Plan reveals his well being care strategy. The New York Occasions. https://www.nytimes.com/2021/01/16/upshot/biden-obamacare-stimulus.html; American rescue PLAN Act funding breakdown. NACo. (2021, July 29). https://www.naco.org/sources/featured/american-rescue-plan-act-funding-breakdown

3 HEALTH INSURANCE MARKETPLACES 2021 OPEN ENROLLMENT REPORT. CMS.gov. (n.d.). https://www.cms.gov/information/doc/health-insurance-exchanges-2021-open-enrollment-report-final.pdf.

4 Finegold, Ok., Conmy, A., Chu, R. C., Bosworth, A., & Sommers, B. D. (2021, February 11). TRENDS IN THE U.S. UNINSURED POPULATION, 2010-2020. HHS.gov. https://aspe.hhs.gov/websites/default/information/personal/pdf/265041/trends-in-the-us-uninsured.pdf.

5 Collins, S. R., Gunja, M. Z., & Aboulafia, G. N. (2020, August 19). U.S. medical health insurance protection in 2020: A looming disaster in affordability. Well being Protection Affordability Disaster 2020 Biennial Survey | Commonwealth Fund. https://www.commonwealthfund.org/publications/issue-briefs/2020/aug/looming-crisis-health-coverage-2020-biennial.

6 COVID enrollment interval. ACA Signups. (n.d.). https://acasignups.web/covid-enrollment-period.

7 Minemyer, P. (2021, Might 24). Common benchmark premiums for ACA alternate Plans decline once more IN 2021: Report. FierceHealthcare. https://www.fiercehealthcare.com/payer/average-benchmark-premiums-for-aca-exchange-plans-decline-again-2021-report#:~:textual content=Averagepercent20benchmarkpercent20premiumspercent20forpercent20plans,fellpercent20bypercent201.7percent25percent20forpercent202021.

8 Saltzman, E. (2017). Demand for Well being Insurance coverage: Proof from the California and Washington ACA Marketplaces. College of Pennsylvania Scholarly Commons. https://repository.upenn.edu/cgi/viewcontent.cgi?article=1140&context=hcmg_papers

9 Abraham, J., Drake, C., Sacks, D. W., & Simon, Ok. I. (2017, July 24). Demand for medical health insurance market plans was extremely elastic in 2014-2015. NBER. https://www.nber.org/papers/w23597.

10 It’s price noting that states that set up their very own marketplaces can recapture the person charge that they have to pay to the federal authorities for collaborating in HealthCare.gov. It is a sizeable evaluation that may save states hundreds of thousands of {dollars}. See: Schwab, R., & Volk, J. A. (2019, June 28). States seeking to run their very own medical health insurance market see alternatives for funding, flexibility. States Trying to Run Personal Insurance coverage Market https://www.commonwealthfund.org/weblog/2019/states-looking-to-run-their-own-health-insurance-marketplace-see-opportunity.

Classes: Well being Coverage, Obamacare

{kind=link}