Jitalia17

In February, I reiterated my purchase ranking on the Simplify Quick-Time period Treasury Futures Technique ETF (NYSEARCA:TUA), noting that 2-year yields have been aligned to the Fed’s projection for year-end Fed Funds charge on the time. Assuming 3 charge cuts have been nonetheless on the desk for 2024, TUA ought to earn again its losses over time from its holdings in treasury payments whereas offering optionality ought to charge cuts happen quicker than anticipated.

Nonetheless, latest occasions have modified my views. Primarily based on incoming knowledge, the American economic system seems to be far stronger than anticipated. This implies the Federal Reserve could delay its rate of interest cuts, or reduce lower than 3 occasions, probably appearing as a headwind for the TUA ETF.

With the bottom case being a stronger U.S. economic system, I don’t imagine buyers ought to wager closely on decrease 2 yr yields. Due to this fact, I’m reducing TUA to a maintain advice.

Temporary Fund Overview

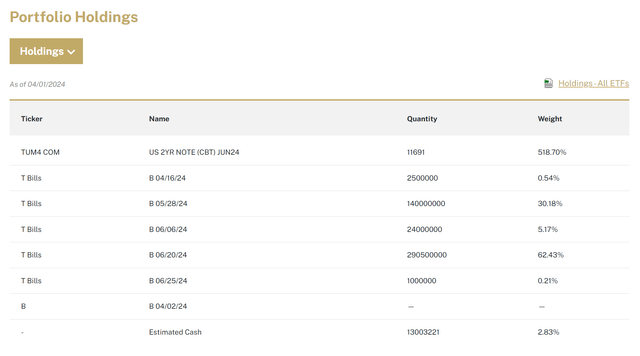

For these new to the fund, the Simplify Quick Time period Treasury Futures Technique ETF is a structured beta fund that holds a roughly 5:1 place in 2-year treasury futures with collateral invested in treasury payments (Determine 1).

Determine 1 – TUA portfolio holdings (simplify.us)

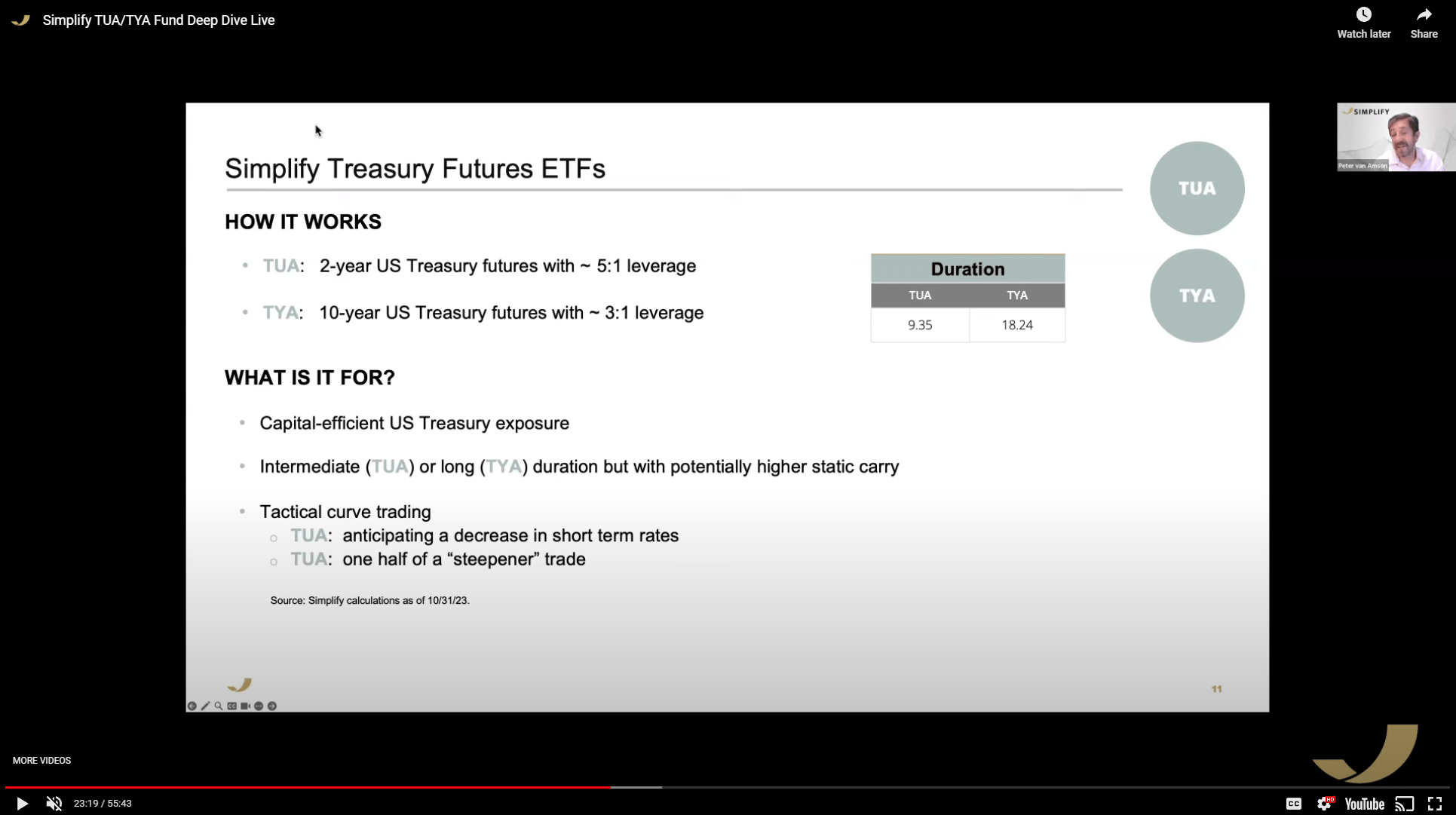

The TUA ETF permit buyers a handy option to wager on a lower in short-term rates of interest (i.e. bull steepener) (Determine 2).

Determine 2 – TUA is beneficial as a curve wager (simplify.us)

Readers who need to be taught extra in regards to the mechanics of the fund are inspired to learn my prior articles or view Simplify TUA/TYA Fund Deep Dive

Swinging Pendulum In Fed Price Lower Expectations

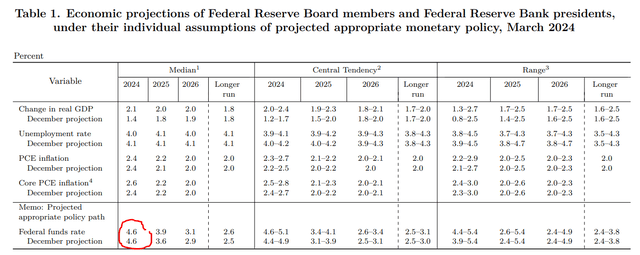

With respect to Fed charge reduce expectations, I’m having doubts as as to if the Fed will truly persist with their December and March projections for 3 charge cuts (Determine 3).

Determine 3 – Fed March Abstract of Financial Projections (Federal Reserve)

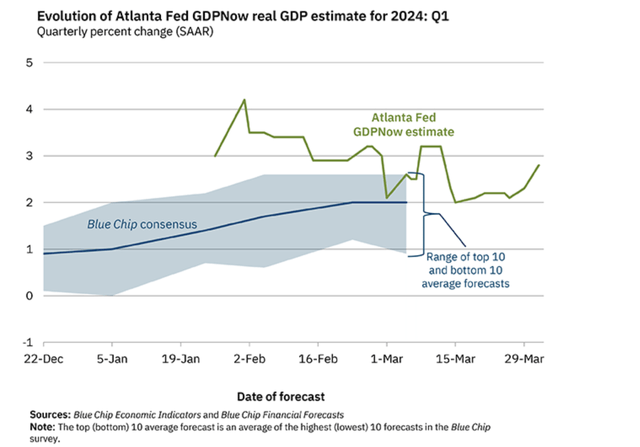

Merely put, latest financial knowledge have been far stronger than I initially anticipated. For instance, the most recent Atlanta Fed GDPNow indicator reveals the U.S. economic system grew at an annualized 2.8% within the first quarter, far stronger than the Fed’s expectations for 2024 full yr progress of two.1% (Determine 4).

Determine 4 – Atlanta Fed GDPNow exhibiting 2.8% progress (Atlanta Fed)

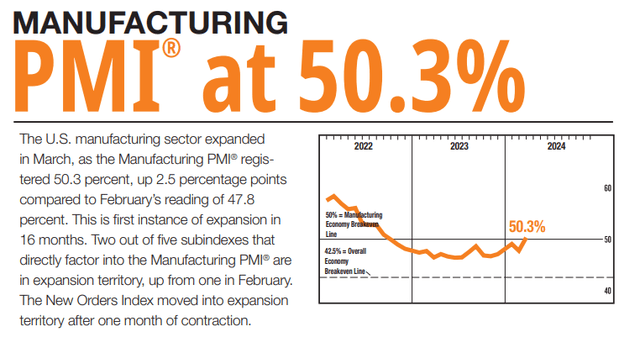

Equally, the March ISM Manufacturing PMI confirmed a studying of fifty.3, far stronger than analyst estimates of 48.5 and the primary enlargement (any studying above 50 designates an enlargement) since November 2022 (Determine 5).

Determine 5 – Manufacturing returning to progress (ismworld.or)

With companies nonetheless rising at a strong tempo, as proven by the February Companies PMI at 52.6%, and manufacturing re-entering enlargement, one may argue that there isn’t a want in any respect for the Federal Reserve to comply with by with their promise of charge cuts.

Will The Fed Ponder Price Hikes As a substitute?

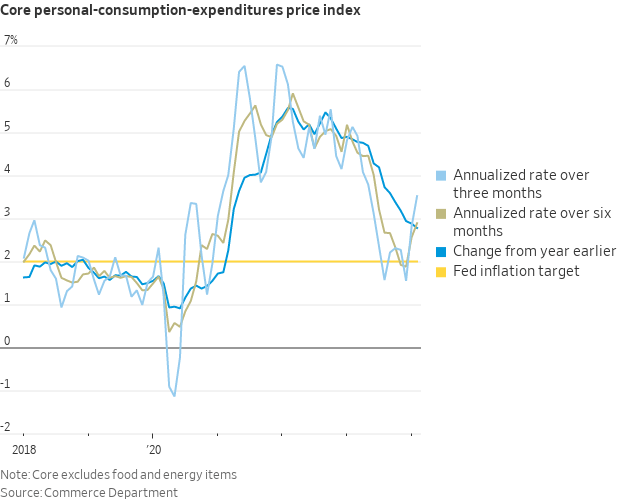

In actual fact, with inflation nonetheless a methods away from the Fed’s 2% goal and with latest indicators of reacceleration, one may even argue that present financial coverage just isn’t tight sufficient and the Fed is failing its pledge to carry inflation sustainably right down to 2% (Determine 6).

Determine 6 – Inflation remains to be a methods away from 2% (WSJ through Nick Timiraos’ X feed)

Maybe as an alternative of rate of interest cuts, the Federal Reserve could need to revisit elevating rates of interest within the coming quarters, if inflation truly reaccelerates larger with the enhancements in exercise and sentiment.

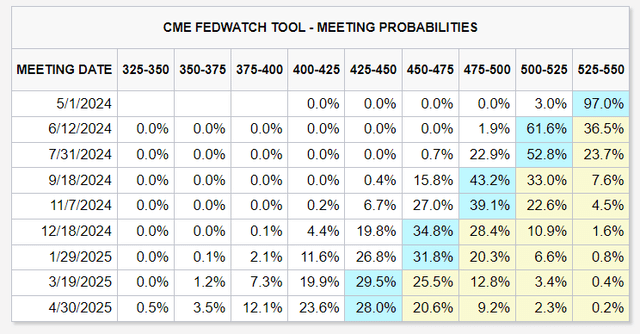

Implied Chance Recommend June Price Lower Is A Coin Flip

market implied chances, the June FOMC assembly is now basically a coin flip, at simply 62% likelihood of a reduce, and the likelihood of three charge cuts in 2024 continues to say no (Determine 7).

Determine 7 – Implied likelihood of charge cuts (CME)

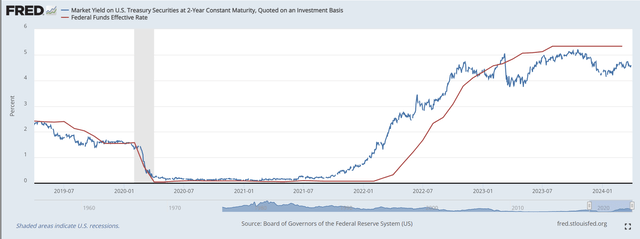

Since 2 yr yields are intently tied to the Fed’s coverage charges, if the variety of anticipated charge cuts are diminished, then 2 yr yields could rise and stress the TUA ETF (Determine 8).

Determine 8 – 2 yr yield is intently tied to Fed Funds charge (St. Louis Fed)

This rise in 2 yr yields has been a headwind for the TUA ETF since January, when the market bought too excited and priced in 6 charge cuts. As these expectations have been ratcheted again to actuality, the TUA have misplaced 4.3% YTD. If the Federal Reserve finally ends up reducing lower than 3 occasions in 2024, then 2 yr yields could rise additional and additional stress TUA’s NAV.

March Distribution Was A Disappointment

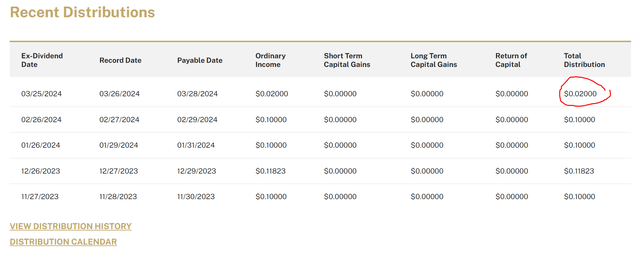

So as to add to unitholder’s distress, TUA’s latest March distribution was a giant disappointment at simply $0.02 / share or an annualized 1.1% (Determine 9).

Determine 9 – March distribution was simply $0.02 (simplify.us)

This quantity was stunning and disappointing as TUA’s collateral is invested in treasury payments and one of many important options of the fund is that buyers get to earn treasury invoice yields whereas betting on a decline within the 2 yr. In actual fact, many readers left indignant feedback in my inbox concerning the decline in TUA’s distribution.

After discussions with Simplify’s consultant, my understanding is that the March distribution reduce was a brief measure to carry TUA’s 12 month distribution yield to be inline with money yields on 2 yr treasuries, and doesn’t have an effect on complete returns of the fund (i.e. the TUA ETF nonetheless earns revenue from treasury payments that will increase NAV).

With trailing 12 month payout of $1.04 or 4.8% in comparison with present 2 yr yield of 4.72%, I believe the catch-up has been carried out and future distributions will resume close to historic ranges. Nonetheless, I concern this fund administration wrinkle could have induced some buyers to panic dump their items when the $0.02 distribution was introduced (Determine 10).

Determine 10 – Some buyers could have panic-dumped TUA as a consequence of distribution reduce (In search of Alpha)

From my expertise as a former fund supervisor, I imagine communication is critically vital between the fund supervisor and buyers, particularly with respect to distributions, as many retirees rely on the money flows from excessive yielding funds just like the TUA to fund their retirements. On this occasion, I imagine Simplify dropped the ball and didn’t correctly talk this ‘true up’ provision in distributions, catching many buyers off-guard.

Low-cost Possibility For What Might Go Mistaken

In abstract, my views on the TUA ETF has shifted from a ‘core holding’ to capitalize on an anticipated decline in short-term rates of interest, to a ‘low-cost possibility’ for what may go unsuitable with the economic system. If the economic system have been to all of a sudden deteriorate, I anticipate the Fed to reply by reducing rates of interest, which might be useful for the TUA ETF. Nonetheless, the bottom case is now a Fed that will reduce lower than 3 occasions this yr, that means there may be danger 2 yr yields keep at present ranges and even goes larger.

Due to this fact, I’m downgrading the TUA ETF to a maintain advice. I feel it’s nonetheless helpful as a positive-carrying wager on decrease 2-year yields, however wouldn’t be a purchaser at present ranges.

{kind=link}