Daniel Grizelj

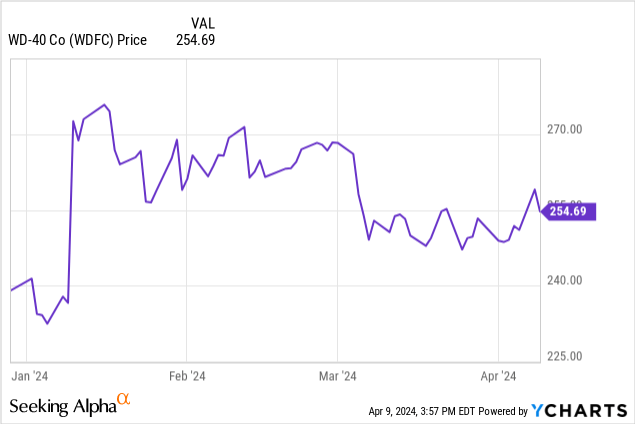

The WD-40 Firm (NASDAQ:WDFC) inventory is a long-term title we now have continued to carry, one in every of our longest-held positions. In our final replace, we continued to recommend holding shares are dear primarily based on valuations metrics. Nonetheless, the inventory has been persistently “overvalued” on many of those metrics. The inventory, regardless of all of the motion within the markets, has held in a good vary the previous few months.

What we now have here’s a very slow-growing title, however one which delivers sluggish and constant long-term returns. There’s a motive we take into account it “previous trustworthy.” Alongside the way in which of those long-term features, we now have seen a dividend persistently paid, and one that’s raised again and again. It has been an incredible title to personal. If we see the inventory pull again some 10%, we’d recommend new cash may add. We are going to probably want a market hiccup for this to happen.

The corporate simply reported Q2 earnings, and nothing we’re seeing within the outcomes adjustments our resolve to carry this long run. Allow us to talk about.

Income progress continues

WD-40 firm persistently and slowly grows gross sales. It enjoys ongoing demand, and internationally there’s extra room for the corporate to develop its geographic footprint. The corporate additionally enjoys pricing energy for its merchandise.

In fiscal Q2, WDFC gross sales had been $139.1 million, up 7% from final 12 months. We had been anticipating gross sales of round $140.0 million, so this was really a slight miss in opposition to our expectations shock. This additionally surpassed consensus by $1.15 million. We had been on the lookout for a excessive single-digit will increase within the prime line, and whereas gross sales got here up just a little brief, it’s largely in line. Nothing to fret about right here. We noticed progress in all areas as soon as once more. General, internet gross sales by location for fiscal Q2 had been 46% within the Americas, 39% in EIMEA, and 15% within the Asia-Pacific area.

Regional breakdown – flattish gross sales within the Americas however power internationally

Gross sales within the Americas solely elevated 1%. There was internet gross sales progress of WD-40 Multi-Use merchandise of $0.6 million, or 1%. That mentioned, we noticed will increase of $1.1 million and $0.7 million, or 12% and a couple of%, in Latin America and the USA, respectively.

Turning to EIMEA, gross sales progress continues to be robust, rising 16%, and this was a results of each worth will increase and promotions put into place by the corporate. We noticed power in France, India, and Iberia. There was additionally a 23% enhance in Specialist merchandise within the area, together with a 17% enhance in Multi-Use merchandise. However pricing was solely a part of the equation, quantity elevated as properly.

Asia-Pacific gross sales have been blended the previous few quarters, because the Asia distributor markets are unstable. Internet gross sales rose 4% versus final 12 months resulting from will increase within the Asia distributor markets, which elevated 7%. It is usually value noting the Australian market noticed a 23% enhance in homecare and cleansing product. General Multi-Use merchandise crept up 3% within the area, whereas Specialist gross sales had been flat.

Margin energy

As a reminder, the WD-40 Firm has a long-term 55% gross margin goal. WD-40 has seen regular enhancements in margin energy of late. Gross margin in fiscal Q2 was 52.4% versus 50.8% a 12 months in the past. This enhance is once more a consequence of pricing will increase, administration slicing prices. This contains WD-40 buying its Brazilian distributor. We additionally discovered within the launch WD-40 will promote its lower-margin homecare and cleansing merchandise in the USA and United Kingdom, which ought to enhance revenue margins. The corporate is getting nearer and nearer to its long-term goal.

The work on normal bills has been useful, however promoting, normal, and administrative bills had been up 10% within the quarter. We want to see higher value controls there. Nonetheless, promoting spend was up 31% from final 12 months, so the corporate is shopping for a few of its personal gross sales to a level.

Regardless of the margin enchancment, the decrease gross sales than anticipated together with a 21% enhance in promoting spend led to a decline in internet revenue to $15.5 million, a lower of 6% from the prior 12 months fiscal quarter. 12 months-to-date, although, internet revenue is up 8%. EPS fell to $1.14 from $1.21 a 12 months in the past, this was really in step with our expectation and a $0.02 miss in opposition to consensus.

Ahead view

Quarters come and so they go. This was not the perfect quarter for the WD-40 Firm, however it was not precisely a dud, both. The corporate is shopping for again shares and continues to spice up its dividend.

As we glance to the 2024 fiscal 12 months, the corporate reiterated most of its outlook, with some enhancements within the outlook. Regardless of EPS declining from final 12 months, EPS for the fiscal 12 months was boosted. Whereas the corporate sees internet gross sales progress of 6-12%, we see 8-11% as extra probably. Margins had been elevated to 51.5% to 53%, up from 51.0% on the low finish. You’ll be able to anticipate internet revenue of $67.7 million and $71.8 million, up from $65 to $70 million at our final protection. And once more, EPS was boosted.

Beforehand, EPS was seen at $4.78 and $5.15. It was upped to $5.00 to $5.30 per share. Oh, and this compares with our EPS expectation on the final replace of $4.95 to $5.25, so expectations are actually extra aligned with our prior forecast.

On the midpoint, that is about 4% progress from final fiscal 12 months. So, whereas WD-40 Firm continues to develop 12 months after 12 months… valuation. At $250 per share, that is practically 50X FWD earnings. That’s costly. Nonetheless, if WDFC shares fall to the $225-$230 ranges, we expect new cash can take into account some shopping for. Shares are more likely to be a bit unstable on this report, with information of gross sales of enterprise traces and revisions to the outlook.

{kind=link}