RobertCrum | Getty Photographs

DETROIT – Skyrocketing auto insurance coverage prices helped contribute to inflation accelerating at a faster-than-expected tempo in March and are including to the ever dearer prices for U.S. automobile house owners.

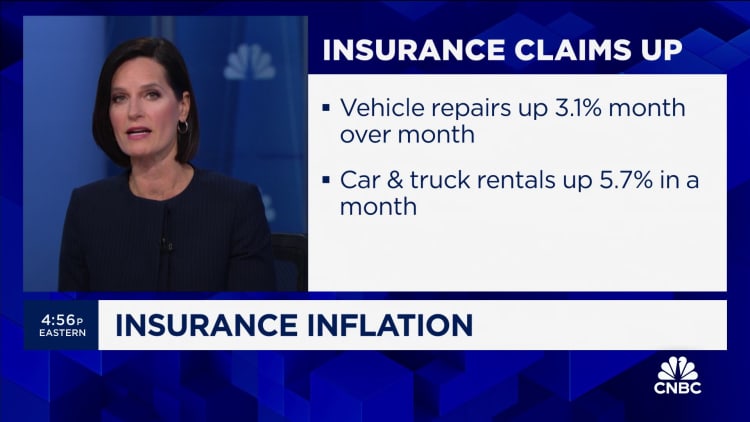

On a month-to-month foundation, automotive insurance coverage costs as a part of the buyer worth index rose by an unadjusted 2.7%, whereas the year-over-year elevated by 22.2%, based on information launched Wednesday. The index is a key inflation gauge and a broad measure of the price of items and companies throughout the economic system.

Auto insurance coverage prices have been on the rise for a while, rising each month as a part of the index since December 2021. Since then, prices have elevated by 45.8%, based on U.S. Bureau of Labor Statistics. Nevertheless, auto insurance coverage stays a small portion of the CPI, with a 2.85% weighting.

The uptick comes on prime of traditionally excessive costs for brand new and used autos because the coronavirus pandemic. It is also turn out to be more and more dearer to restore autos because of provide chain shortages, mechanic wage will increase and extra applied sciences in autos resembling microprocessors, cameras and different sensors — all of which contribute to increased automobile and insurance coverage prices.

“There’s not a single issue, however I feel the largest issue is a mixture of latest automobiles and dearer, so when you complete your automotive the substitute value is admittedly excessive and a fender bender could be very costly proper now,” stated Sean Tucker, senior editor at automobile valuation and automotive analysis firm Kelley Blue E book. “The expertise within the automobiles, it is a very particular downside.”

As a substitute of getting to exchange a plastic or metal bumper on many autos, a easy fender bender can now harm cameras, proximity sensors and ranging different applied sciences used for newer security options and instruments resembling cruise management, parking and emergency braking.

“Premiums have been on the rise as a result of the price of what goes into auto insurance coverage has been rising,” David Sampson, CEO and president of the American Property Casualty Insurance coverage Affiliation, informed CNBC. “There is a lengthy lag time between when the traits emerge and firms see these loss traits current. It then takes time for them to construct that into their charge utility filings.”

Earlier this 12 months, Sampson himself had slight harm to a bumper on a 2024 pickup truck on his property that he says was quoted to value him $1,800 to restore or exchange.

“The entire expertise that we have come to depend on makes makes the substitute or restore of those autos actually, actually, pricey,” stated Sampson, whose group is the first nationwide commerce affiliation for dwelling, auto and enterprise insurers.

The insurance coverage value will increase on inflation come greater than two years after the Biden administration largely blamed used automotive costs for pushing inflation increased in January 2022.

Mitchell, an automotive software program supplier specializing in collision restore and auto insurance coverage sectors, stated restore prices had been rising at an annual charge of about 3.5% to five% previous to the coronavirus pandemic. As of 2022, the will increase have been at 10% or above, with the typical repairable estimate for a automobile at $4,721 in 2023.

Customers and firms alike aren’t pleased with the will increase. J.D. Energy in June reported auto insurers misplaced a median of 12 cents on each greenback of premium they collected in 2022 — the worst efficiency in additional than 20 years — main them to lift charges on the expense of buyer satisfaction.

“What I at all times remind of us is that insurance coverage relies on actuarial science, so it isn’t a case of insurers simply deciding that they wish to enhance premiums,” Sampson stated. “The filings must be based mostly on actuarial loss traits of their charge purposes in every state.”

The price of automobile insurance coverage — which is necessary in nearly each state — varies by supplier, driver, protection and site. Practically all states have minimal necessities for legal responsibility protection, however there are a selection of different coverages which will or might not be required in a particular state, based on insurance coverage supplier Progressive.

The listing of non-compulsory and necessary protection areas will be fairly lengthy and costly for drivers, which has led many insurance coverage firms to supply usage-based insurance coverage, or UBI, applications that base the price of a coverage on a driver’s behaviors utilizing telematics information.

Prospects who’re new to an insurer have a UBI participation charge of 26%, based on the J.D. Energy’s U.S. Auto Insurance coverage Examine from June.

The examine, in its 24th 12 months, discovered UBI utilization greater than doubled from 2016 to 2023, with 17% of auto insurance coverage clients collaborating in such applications. Worth satisfaction amongst clients collaborating in these applications is 59 factors increased on common than amongst non-participants, based on J.D. Energy.

Utilization in such applications is simply anticipated to extend as prices rise and insurers provide reductions or particular costs for safer drivers, based on insurance coverage firms.

Based mostly on J.D. Energy’s survey, UBI applications from Geico, Progressive, State Farm and Liberty Mutual had been ranked above common by clients. USAA, which companies all branches of the navy and their households, ranked the best.

J.D. Energy’s examine additionally discovered the price will increase have led to a greater than 20-year low in buyer satisfaction with auto insurance coverage firms.

“General buyer satisfaction with auto insurers has plummeted this 12 months, as insurers and drivers come nose to nose with the realities of the economic system,” Mark Garrett, director of insurance coverage intelligence at J.D. Energy, stated in a June launch.

— CNBC’s Robert Ferris and Jeff Cox contributed to this text.

{kind=link}