The interval between now and year-end marks a traditionally bullish ultimate stretch of the 12 months for U.S. shares, significantly simply earlier than and after Christmas. The query for buyers is whether or not favorable seasonal components will likely be outweighed by financial fundamentals.

The momentum towards a year-end rush to shares appears to solely be getting stronger now that the S&P 500

SPX,

has rallied 12.6% from its October low — fueled by better-than-expected inflation studies for final month and business-friendly Republicans’ slim win of the Home.

Dow industrials

DJIA,

have jumped practically 20% since a late-September low, on the cusp of the brink that may mark an exit from a bear market, whereas the Nasdaq Composite has put in a middling efficiency as buyers stay in a wait-and-see crouch in regards to the Federal Reserve’s December fee resolution, additional inflation information, and geopolitical dangers abroad.

Main indexes logged features in a holiday-shortened Thanksgiving week, with the Dow up 1.8%, the S&P 500 gaining 1.5% and the Nasdaq Composite advancing 0.7%.

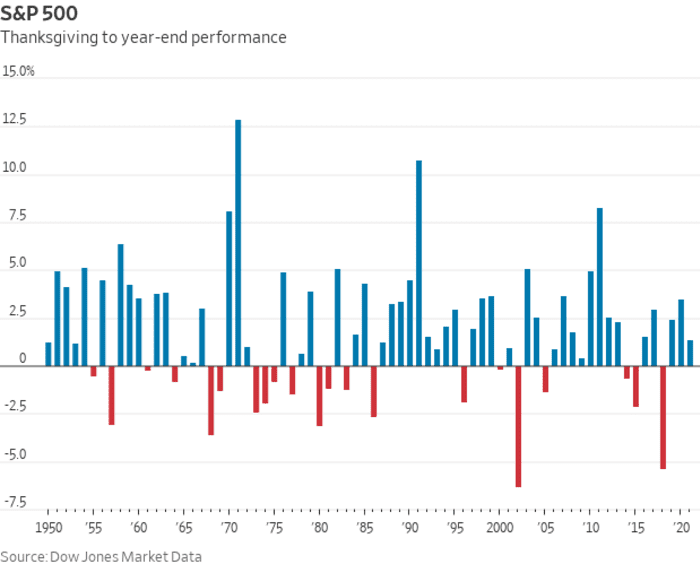

After which there’s a seasonal end-of-year tailwind. In keeping with Dow Jones Market Knowledge, the S&P 500 has risen 71% of the time within the stretch from Thanksgiving to year-end, based mostly on figures going again to 1950. On common, the large-cap benchmark has risen 1.8% in that interval. Such information generally is a tough information for buyers, however isn’t any assure of efficiency in a given 12 months, because the purple traces within the chart under illustrate.

Dow Jones Market Knowledge

And that favorable seasonal sample might be set to collide with fears that 2023 may carry stagflation: the worst-of-all-possible financial outcomes and one which buyers could be hard-pressed to be ready for. Stagflation is outlined as a interval of gradual financial development plus persistently excessive inflation, a dynamic which will already be below means within the U.S.

Warnings of a probably deep U.S. recession forward are flashing recurrently within the bond market, the place the broadly adopted unfold between 2-

TMUBMUSD02Y,

and 10-year Treasury yields

TMUBMUSD10Y,

stays close to minus 80 foundation factors — which means the 10-year fee stands practically 0.8 proportion level under the 2-year yield. The curve prior to now week hit its most deeply inverted since 1981. Such inversions are seen as a dependable recession indicator.

U.S. development turned constructive within the third quarter and inflation seems to be easing, based mostly on October’s consumer-price index during which the annual headline fee dropped to 7.7% from 8.2% beforehand. But worth features should not coming off quick sufficient for the Federal Reserve to utterly abandon aggressive fee hikes, which may tip the world’s largest financial system right into a downturn.

“The tough half for buyers in a stagflation state of affairs could be confusion over the place to speculate,” stated Mark Neuman, founding father of Atlanta-based Constrained Capital and creator of the ESG Orphans Index which tracks shares with $3 trillion in mixed market capitalization.

That’s a reversal from the market tendencies which prevailed for a lot of this 12 months and “is due partly to excessive investor positioning in these trades being flipped by the worry of lacking out [on] a year-end rally,” stated Jason Draho, head of asset allocation for the Americas at UBS World Wealth Administration.

Including to the previous month’s bullish tone in shares has been October’s stronger-than-expected retail gross sales plus a weaker-than-expected producer-price report, each of which present that “the financial system is holding up effectively, regardless of the continuing rise in short-term charges,” stated Sam Stovall, chief funding strategist for CFRA Analysis in New York.

“Seasonality will supply a little bit of a carry to shares towards the top of the 12 months, and I feel buyers predict the Federal Reserve to hike by 50 foundation factors in December and possibly not be all that hawkish of their assertion,” Stovall stated by way of telephone. “Proper now, the inventory market is assuming we don’t fall right into a recession or, if we do have a recession, will probably be delicate and that the Fed will doubtless decrease rates of interest within the latter a part of 2023.”

He stated that CFRA’s financial outlook requires the U.S. financial system to narrowly miss a recession, but nonetheless fall into stagflation, adopted by a U-shaped, reasonably than a V-shaped, restoration.

“If the course of inflation continues to be downward — that’s, inflation steadily however persistently falling — that may be sufficient to make buyers really feel fairly good in my view,” Stovall advised MarketWatch. “As well as, we predict to see an enchancment in company revenue development as we transfer into 2023.”

In keeping with Stephen Suttmeier, chief fairness technical strategist for BofA Securities, the final 10 buying and selling classes of December via the primary 10 classes of January has confirmed to be a bullish interval for the S&P 500, time and time once more: The index is up 72% of the time on a median return of 1.19% over the past 10 buying and selling classes of December, he stated. That power tends to hold over into the brand new 12 months, with the S&P 500 up 64% of the time on a median return of 0.72% throughout the first 10 days of January.

Mark Hulbert: ‘Santa Claus rally’ for shares is probably going this 12 months — however you gained’t be opening presents till after Christmas

These year-end seasonal components run alongside a well known sample that has seen shares put of their finest efficiency over a six-month stretch starting in November.

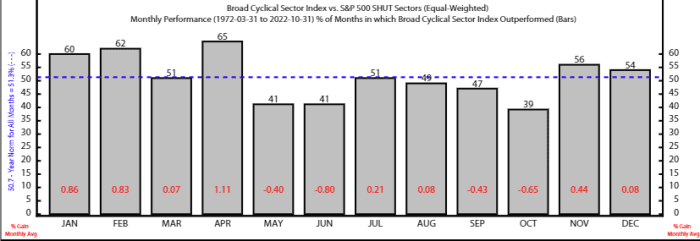

The six-month interval from November to April tends to significantly favor equities throughout a swath of cyclical shares, in line with strategist Rob Anderson and analyst Thanh Nguyen at Ned Davis Analysis. NDR’s Broad Cyclical Index, which incorporates the economic, consumer-discretionary and supplies sectors, has outperformed a defensive basket made up of staples, healthcare, utility and telecommunications corporations, on common, between these six months since 1972.

In addition they stated that technical causes help the case for a year-end rally in U.S. shares, whereas noting that “outdoors forces can overwhelm seasonal tendencies.”

Supply: Ned Davis Analysis

The highlights for the week forward embrace Thursday’s launch of the Fed’s most popular inflation gauge for October and Friday’s nonfarm payrolls report for November.

On Monday, MarketWatch interviews St. Louis Fed President James Bullard. Tuesday brings the S&P Case-Shiller U.S. residence worth index, the FHFA U.S. residence worth index, and November’s consumer-confidence index.

Don’t miss: Fed’s Bullard set to speak inflation, rates of interest in MarketWatch Q&A Monday

Wednesday’s main information releases embrace the ADP employment report, a revision to third-quarter GDP, the Chicago buying managers index, updates on job openings and quits for October, and the Fed’s Beige E-book report. Fed Chairman Jerome Powell can also be set to talk on the Brookings Establishment.

Thursday’s information batch contains weekly jobless claims, October’s personal-consumption expenditures worth index, the S&P U.S. manufacturing PMI, and ISM’s manufacturing index. On Friday, November’s nonfarm payrolls information and unemployment fee are launched.