Stephen Swintek/DigitalVision by way of Getty Photographs

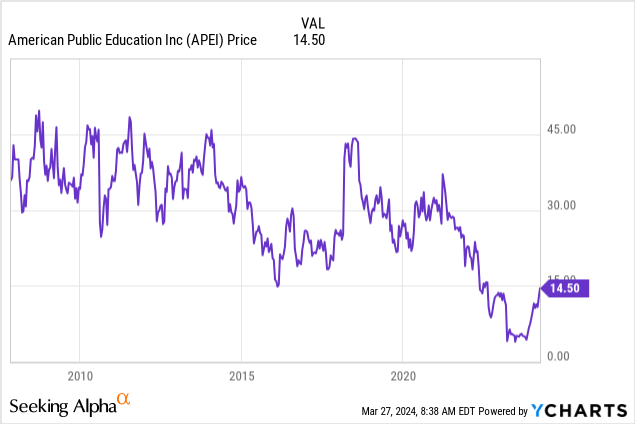

Whereas the inventory worth of American Public Schooling, Inc. (NASDAQ:APEI) has tripled within the final six months, it’s nonetheless down greater than 50% during the last 5 years. Is the current surge the start of a profitable turnaround? Or reasonably, one further episode within the long-lasting march of destroying shareholders’ worth at a fee of damaging 7% a 12 months? Let’s discover out.

I am going to first give a brief overview of APEI’s actions earlier than discussing why the inventory worth remained flat between its IPO in 2007 and 2020. Then, I am going to talk about why the inventory has plummeted since COVID-19 however has elevated not too long ago. Lastly, I am going to offer you my outlook for 2024 and past.

What does APEI do?

American Public Schooling, Inc. is the holding firm above a number of universities, every primarily centered on grownup learners.

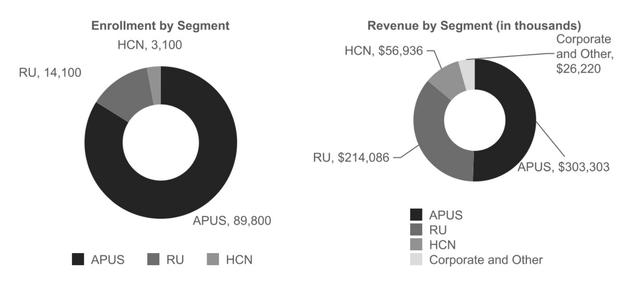

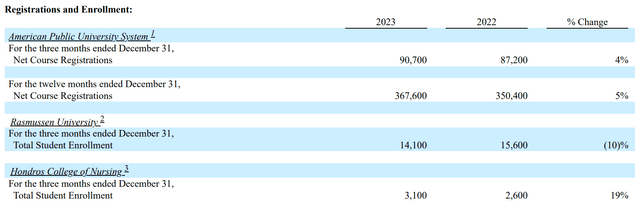

- The most important college within the portfolio is the American Public College System. It’s a web based college that caters to 89,800 grownup learners, together with army personnel (66% of scholars) and veterans (11% of scholars). Based in 1991 as a graduate establishment for army officers, APUS has expanded its choices to a broader viewers, emphasizing schooling for these in service roles. At the moment, it contains the American Navy College (AMU) for army and associated communities and the American Public College (APU) for professionals in fields like nursing and enterprise.

- In 2013, APEI acquired Hondros Faculty of Nursing (HCN). This faculty educates round 3,100 nursing college students throughout eight campuses in three states, providing PN (65% of scholars) and ADN (35% of scholars) levels with direct entry choices for certified college students.

- In 2021, APEI additionally acquired Rasmussen College (then referred to as Rasmussen Faculty). This College provides nursing and well being sciences schooling to over 14,100 college students throughout 22 campuses and on-line. Initially centered on enterprise schooling, RU expanded into healthcare in 2006, now providing a variety of nursing levels from pre-licensure to Doctorate of Nurse Follow. Roughly 5,700 college students are enrolled in nursing applications, with most pursuing pre-licensure levels.

- Lastly, in 2022, APEI accomplished its most up-to-date acquisition, taking on Graduate Faculty USA. GSUSA supplies profession schooling to the federal and public workforce, serving over 100 federal businesses. It provides over 300 programs in skilled improvement and management by way of on-line and in-person coaching. In 2023, GSUSA educated over 27,000 folks.

As such, by way of these acquisitions, APEI has diversified its course choices away from army coaching and in the direction of nursing. Nonetheless, an important College stays the APUS section, each by way of enrollment as by way of income (and in earnings, as I’ll come again on down under):

This fall earnings APEI

Why was the inventory flat between 2007 and 2020?

The APUS universities had been reportedly of top quality and among the many finest for-profit universities, in keeping with a U.S. Senate investigation in 2012.

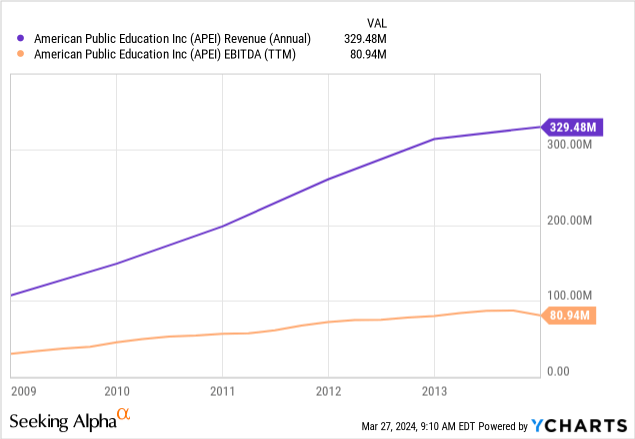

As such, up till 2014, the variety of enrolled college students exploded. APUS had solely round 15.5k enrolled college students in 2006, which elevated to 78k in 2010 and 112k in 2013.

Alongside the identical line, income elevated from $107M in 2008 to $330M in 2013, whereas EBIT nearly tripled from $25M to $67M. All with out diluting shareholders.

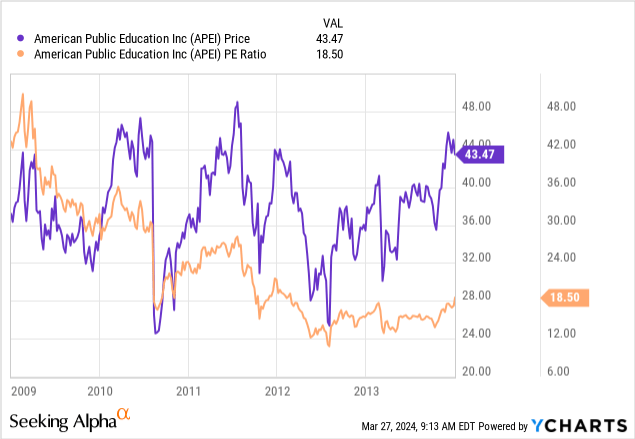

The inventory, nonetheless, remained flat. It is because traders had valued APEI in 2009 as a progress inventory, valuing it at a PE of >40x. On the finish of 2013, this valuation had come all the way down to a PE of 18x.

At 18x, the market appropriately priced in years of decrease progress. Administration tried to fight this and determined to hunt for inorganic progress. As mentioned above, it acquired HCN in 2013. They paid 46 million {dollars}, which was affordable provided that Hondros remodeled $3M in working earnings.

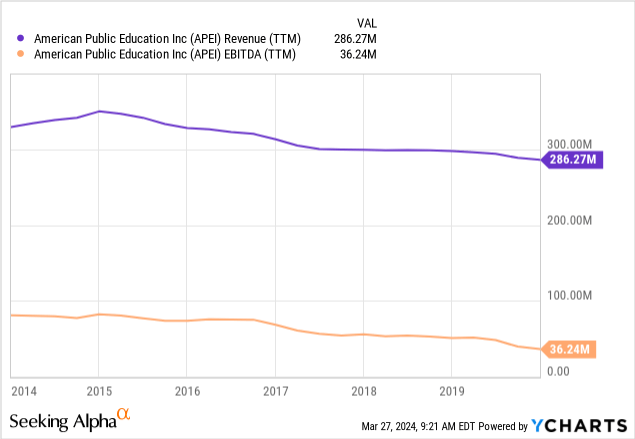

Nevertheless, this didn’t repair the underlying problem: the expansion in APEI’s principal asset, APUS, had stopped. Over the following years, between 2013 and 2020, no additional acquisitions can be made, and income declined each single 12 months by mid-single-digit. EBITDA would even halve from $80M to $36M:

As administration purchased again round 20% of its shares over these 5 years, and valuation elevated a bit to 22x PE, the inventory worth traded sideways for an additional 5 years up till 20% of its shares over these 5 years, and valuation elevated a bit to 22x PE, the inventory worth traded sideways for an additional 5 years up till 2020.

Why did the inventory plummet between 2020 and 2023?

In 2019, Angla Selden joined the corporate as CEO. She has expertise in on-line schooling and academic software program. It was hoped she may re-invigorate APEI’s progress.

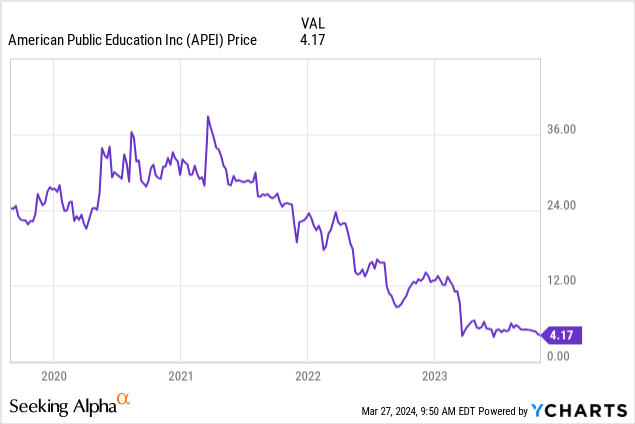

Not lengthy after her appointment, Covid-19 compelled universities to close down and go into lockdowns. Buyers believed this to be a singular alternative for APEI, and APUS extra particularly, given it’s fully on-line. As such, the inventory worth surged 40% throughout 2020, far outpacing the general market.

Certainly, efficiency in 2020 was robust, with income lastly rising once more (12%) and margins enhancing significantly (EBIT margin improved from 7 to 9%). Within the wake of those robust outcomes, CEO Selden determined to make use of the agency’s robust money steadiness to make sure APEI’s progress for the years to come back.

In 2021, she acquired Rasmussen College for $329 million, consisting of $300 million in money and $29 million of non-voting most well-liked inventory. One 12 months later, in 2022, she acquired G.S.USA for $1 million.

The acquisition of RU can be a nightmare and the (nearly) sole motive for the horrendous inventory efficiency since.

In 2021, RU’s enrollment numbers dropped by 3%. In 2022, it dropped a further 12 (!) p.c and an extra 6% in 2023. As such, whereas the College made a revenue of $1.6M in 2021, it turned a lack of $20M in 2022 and $39M in 2023 (even after ignoring the goodwill amortization)! Moreover, company bills additionally elevated in making an attempt to handle the now larger group.

By the tip of October 2023, the inventory worth had collapsed to 4$ – one-sixth of the value when Selden grew to become CEO simply 4 years prior. The acquisition has, thus, been nothing in need of disastrous.

Why the resurgence in 2024?

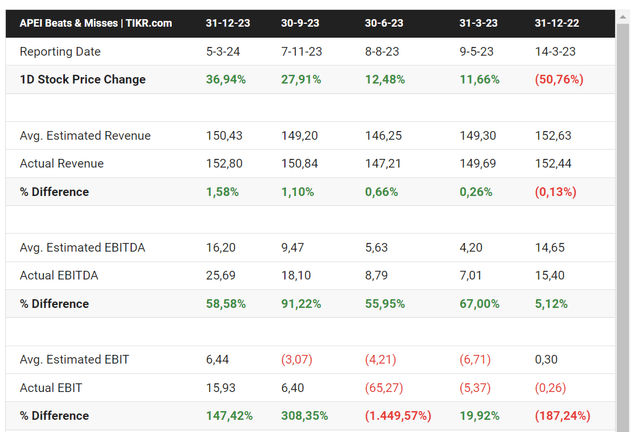

After posting horrendous numbers all through 2022 and into 2023, expectations had change into reasonably depressed. Even after the share worth had been slashed by the start of 2023, the inventory halved after This fall 22 numbers had been launched. This resulted in additional downward changes of expectations. These had been too pessimistic, in hindsight, and traders have been relieved by the numbers within the prior 4 quarters:

TIKR

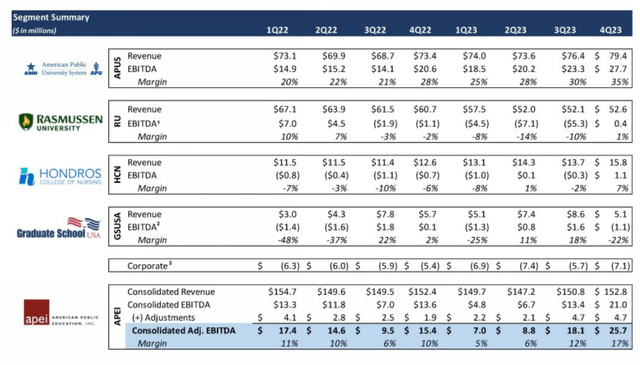

This fall 2023 was even fairly good: adj. EBITDA margin got here in at 17% on the again of higher price self-discipline. Even Rasmussen College turned out to be “worthwhile”:

APEI This fall earnings

Furthermore, administration has guided for an EBITDA margin larger than 10% within the seasonally weaker Q1 2024. That is not all. By the tip of 2024, the costly IT-support contract with Collegis will expire. Additionally, APEI has been making prices to transition this help in-house. Most of those prices will cease from This fall 2024 onwards.

What subsequent?

APEI has finished 2 very giant goodwill impairments up to now two years, such that just about the entire goodwill ensuing from the acquisition of Rasmussen College has been written off. On the similar time, it has elevated tuition charges, lowered advertising bills, and stopped the costly contract with Collegis as a result of it believes it will probably do advertising and IT help in-house. Furthermore, enrollments are rising once more in APUS:

APEI This fall earnings

As such, as administration has guided for an EBITDA margin of 10% in Q1 2024, I count on that the margin for the complete 12 months will exceed 10%. Administration has guided a bit decrease however defined within the name that they “actually wish to be sure [they]’re not being too aggressive on that finish”. At a ten% margin, EBITDA must be $62M. On the similar time, they’re guiding for 20M in CapEx (higher finish). As such, web of SBC, free money circulation must be $40M in 2024.

In 2025, I imagine that FCF will enhance additional as a result of:

- I think administration will stick this time to having price self-discipline;

- The Collegis-costs will likely be excluded for the complete fiscal 12 months, in addition to the transition prices;

- Altering Illinois laws must also enable most Rasmussen College campuses to enroll extra college students;

- APUS ought to proceed on its not too long ago re-found progress trajectory.

As such, at a market cap of $253M, APEI trades at lower than 6x ahead (conservative) FCF, which is prone to have bottomed. Friends equivalent to Common Technical Institute (UTI) or Perdoceo Schooling Corp. (PRDO) commerce at 14x FCF. Given the inventory’s current robust momentum, I really feel like there’s nonetheless loads of room for traders to purchase into this restoration play.

.jpg)

{kind=link}