HJBC/iStock Editorial through Getty Photos

Right here on the Lab, we like utility firms, and our group just lately upgraded Enel and E.ON. In the present day, we’re again to touch upon Engie (OTCPK:ENGIY). On the French participant, we had been in a Wait-and-See mode, and as reported in our final evaluation, we had been anticipating a reassuring outlook and a simplified enterprise mannequin earlier than altering our valuation. That mentioned, earlier than commenting on the corporate, we should always take a step again and have a look at the sector.

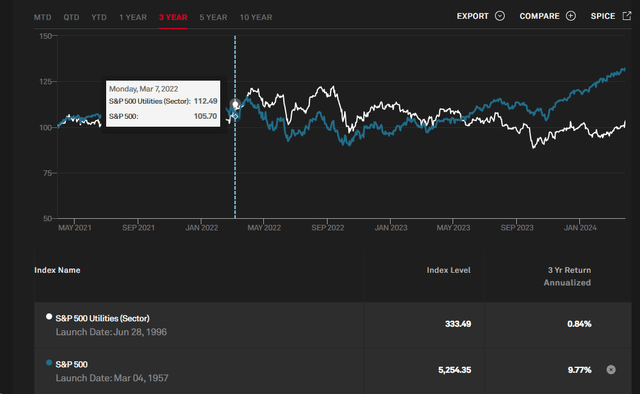

Trying on the utilities sector, it’s evident that it has been underperforming the market since 2022 (Fig 1). Contemplating the continuing Russia-Ukraine battle and its repercussions on the power worth, we consider the sector may benefit from decrease rates of interest. Wall Road is awaiting communications from main central banks on the timing of first-rate cuts, that are anticipated to start in June. Whereas June would possibly be a great time, nothing is about but. ECB and FED argue that their choices will rely upon financial and inflation information. Given the sector’s weak development and traditionally excessive and steady dividends, even when we’re not forecasting a June lower, we consider built-in utility gamers will doubtless profit from a decline in long-term charges. As well as, till very just lately, utilities had been thought-about akin to high-quality bonds. Nonetheless, with electrical energy grids scaling to unprecedented ranges, we see higher development in low-risk regulated belongings than earlier than. This was already evident in Engie Fiscal Yr 2023 outcomes.

S&P 500 Utilities Index Evolution

Supply: S&P 500 Utilities – Fig 1

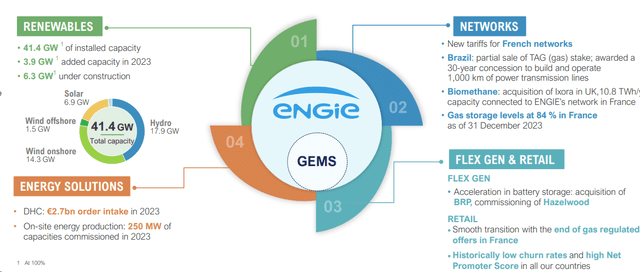

For our new readers, Engie SA is a France-based international power participant that operates by 4 divisions: renewables, networks, power options, and flex gen & retail. As well as, Engie has nuclear operations in Belgium. Right here on the Lab, we beforehand anticipated increased provisions for the nuclear asset life extension in addition to its waste liabilities. Nonetheless, we consider the corporate is now more likely to considerably de-risk itself.

Engie 4 Core Segments

Supply: Engie Fiscal Yr 2023 outcomes presentation – Fig 2

Why are we constructive?

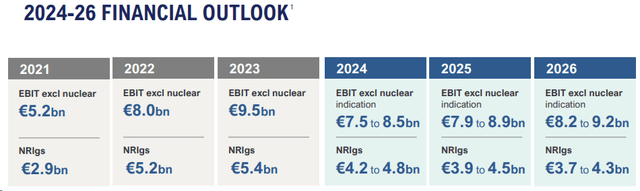

- With the This autumn and 2023 FY outcomes, the corporate reassured traders with constructive medium-term steering (Fig 3). After checking Engie’s financials and forecasting decrease energy costs, we report that the corporate’s low-end outlook remains to be above consensus. Due to this fact, this would possibly positively affect its inventory worth evolution;

- Engie has a sexy capital remuneration coverage. Intimately, the corporate’s board will suggest a DPS of €1.43 per share. On the present market worth, this represents a dividend yield of 9.2%. Engie has a shareholders remuneration set with a 65/75% payout ratio and a minimal dividend flooring of €0.65 till 2026 (Fig 4). Due to this fact, in a depressed situation, there may be draw back safety. As a reminder, the corporate goes ex-dividend on Could 2nd. In our forecast, we anticipate a declining DPS set at €1.18, €1.16, and €1.17 for 2024-2025-2026;

-

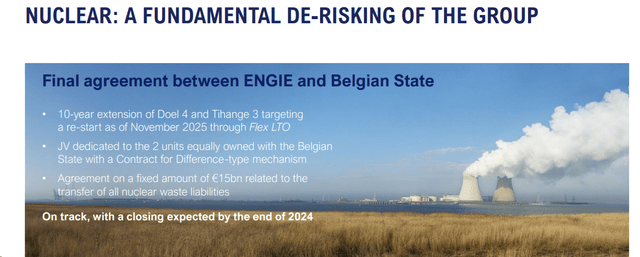

Engie signed a last settlement on the Belgian nuclear plan and essentially de-risked the Group portfolio (Fig 5). The corporate now expects a €0.2-0.4 billion core working revenue contribution from nuclear publish 2026. This eradicated Engie’s longstanding uncertainty on nuclear waste liabilities. Right here on the Lab, we consider this additionally simplified the group construction and eliminated one other overhang;

-

Key to report is Engie’s structural development anticipated within the upcoming years. We consider the market has missed the corporate’s EBIT development. In our supportive ahead view, Engie’s development engines might be batteries and renewable power improvement, that are very effectively supported by the corporate’s resilient incomes generator, i.e., the community division. Trying again, we should always report that the corporate delivered a core working revenue CAGR of 13% between 2021 and 2023. Even when we’re forecasting a gradual deterioration of the group’s commodity-driven earnings, Engie’s new community core working revenue steering helps our monetary estimates;

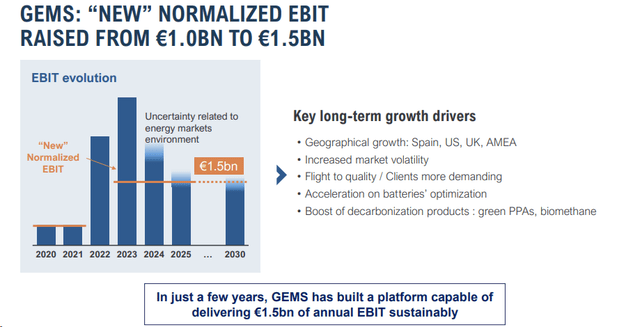

- Trying on the GEMS & Retail division (Fig 6), we consider the corporate forecasts cautious steering. We now have a distinct view supported by three key takeaways: 1) there may be increased volatility post-COVID/Ukraine battle on power worth; 2) we consider there are increased margins on battery storage belongings; and three) the retail division is extra worthwhile attributable to increased demand for renewable electrical energy demand (from B2B purchasers);

- With commodity-driven income normalizing and Engie’s nuclear EBITDA technology lowered, we anticipate Engie’s onerous work to bear fruit. Right here on the Lab, we mission a declining EBITDA in our three-year seen interval. In numbers, our 2024-2025-2026 EBITDA is about at €14.54, €14.46, and €14.14 billion, respectively. Following an aggressive CAPEX plan, our EBIT is forecasted at €9.07, €8.89, and €8.96 billion with an EPS of €1.81, €1.66, and €1.67;

- In addition to, even when we’re not speculating on portfolio rotation, we all know disposal might play a vital position in housekeeping. This additionally supplies flexibility on the web debt profile. In our three-year seen interval, we anticipated a monetary leverage under 4x.

Engie 2024-2026 Outlook

Fig 3

Engie DPS Ground

Fig 4

Engie Nuclear Replace

Fig 5

Engie GEMS new estimates

Fig 6

Valuation

We just lately valued Enel, so we’re making the most of our earlier publication. Certainly, wanting on the sector, the EU-integrated firms commerce with a P/E and EV/EBITDA at 14.86x and >7x, respectively. In our 2024 numbers, Engie trades at a P/E of 8.56x with an EV/EBITDA of roughly 5.5x. At this stage, we see restricted worth granted by the market to Engie’s development prospects. As well as, the networks/GEMS upgrades will doubtless permit the French participant to climate decrease power costs extra gracefully. French fuel storage ranges are fairly excessive, and the following 2024/2025 winter ought to be moderately safe from a provide standpoint. Extra importantly, the overhang on Nuclear liabilities has been eliminated.

We see no motive why Engie ought to commerce at a reduction. That mentioned, making use of a 10x P/E attributable to a decrease EPS evolution anticipated till 2026, we worth Engie with a goal worth of €18.1 per share ($19.5 in ADR). This implies a purchase score valuation with an anticipated complete return of roughly 26% in one-year ahead estimates.

Dangers

Engie’s vital dangers to our goal worth embody a low and extended power worth atmosphere, CAPEX delay with no development in photo voltaic and wind internet capability additions, decrease credit score for battery and renewables development past 2024, GEMS EBIT again to the pre-energy disaster degree, and provisions within the retail division. Greater rates of interest additionally negatively affect Engie.

Conclusion

We consider Engie is about to outperform the market in 2024. Our evaluation is supported by 1) a sexy valuation, 2) earnings defensiveness pushed by the community division, 3) decrease dangers on Nuclear, and 4) a simplified construction. Even when we’re not speculating on fee cuts, the sector is delicate to curiosity actions, and we consider we’re at fee decide. Due to this fact, Engie is now a Mare Proof Lab’s high decide.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}