Sundry Images

Thesis

Over the previous 12 months, the value of nVent Electrical plc (NYSE:NVT) rose by greater than 78%, making it a capital beneficial properties hero. The corporate has been an aggressive progress inventory because it turned impartial and publicly traded in 2018.

The supplier {of electrical} connections and safety options ought to develop once more this 12 months, however I count on the tempo to sluggish and the share value progress to be considerably muted consequently.

Nonetheless, this can be a sturdy firm and I count on the share value to climb by one other 6.29% over the following 12 months and price it a Purchase. It has administration with progress ambitions, a plan for driving progress, and the monetary assets to implement it.

About nVent

In its 10-Ok for 2023, the corporate describes itself as,

“a number one world supplier {of electrical} connection and safety options.” and “Our broad vary of merchandise and options help industrial, business and residential, infrastructure, and vitality purposes all over the world. Our options assist our clients enhance vitality effectivity, guarantee resiliency and safety, enhance buyer productiveness, design for prolonged lifespan and serviceability, improve security and contribute to extra sustainable operations.”

Its first predecessor firm was fashioned in 1894; since then, it has grown and expanded by natural progress and acquisitions. It has additionally been by numerous iterations as an organization. Most just lately, it was spun off from Pentair plc (PNR), which was separating its water and electrical companies. It then turned an impartial, publicly traded firm that began buying and selling on the New York Inventory Change in 2018.

It additionally reported that it affords a portfolio of enclosures, electrical fastening options, and thermal administration options. The Our Spark administration system ties numerous components of the corporate along with 5 standards that outline the way it operates:

- Individuals refers to its administration and employees, and its efforts to advance their careers.

- Development is known as the inspiration of Our Spark, so as to add shareholder, buyer and worker worth.

- Lean is a steady enchancment technique aimed toward lowering waste and accelerating operations.

- Digital includes each its merchandise and the way it does enterprise, for higher buyer and worker experiences.

- Velocity refers back to the purpose of dashing up what it does for workers and clients.

nVent operates by three segments: Enclosures, Electrical & Fastening Options, and Thermal Administration.

On the shut on Monday, March 25, 2024, its share value was $74.03 and it had a market cap of $12.16 billion.

Competitors and aggressive benefits

The corporate faces vital competitors and rivals, noting within the 10-Ok that its markets are geographically various and extremely aggressive. It argued that its success is dependent upon components similar to technical experience, repute for high quality and reliability, timeliness of supply, and contractual phrases and value.

A web-based seek for electrical enclosure producers within the U.S. brings up the names of Schneider Electrical S.E. (OTCPK:SBGSF) and Emerson Electrical Co. (EMR).

For electrical fasteners, distinguished rivals are Schweitzer Engineering Laboratories, MKE Engineering, and Ablerex Electronics.

Business leaders in thermal administration embrace Parker-Hannifin Company (PH), Superior Cooling Applied sciences Inc., and Honeywell Worldwide Inc. (HON).

nVent seems to have no less than a few aggressive benefits. First, it has a portfolio of services throughout the electrical business, which ought to help in aggressive intelligence, cross-selling, and different alternatives.

Second, it’s a world participant, which means it may well diversify its gross sales, alternate experience amongst completely different markets, and has the information and experience to broaden into much more international locations.

Margins

Its margins counsel the agency has aggressive benefits and a robust aggressive moat:

- Gross margin [TTM]: 49.99%, in contrast with 30.52% for the Industrials sector median.

- EBITDA margin [TTM]: 20.01% versus 9.99% for the sector.

- Internet earnings margin [TTM]: 69.33%, which is way larger than the sector’s 5.97% median.

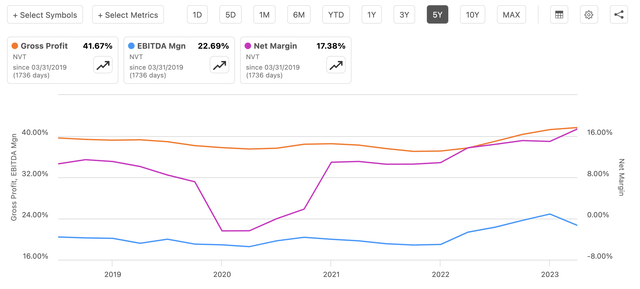

Over the previous 5 years, the gross and EBITDA margins have been secure, whereas the web earnings margin has shot up:

NVT Margins chart (Looking for Alpha)

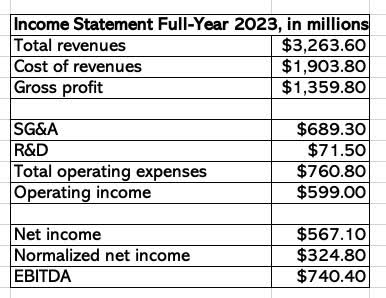

This simplified earnings assertion exhibits the development from prime line to backside line.

NVT Simplified Earnings Assertion (Writer)

The power of the margins displays no less than a few components. First, the corporate’s Lean initiative, which has been outlined as maximizing worth whereas minimizing waste. It originated at Toyota Motor Company (TM) in Japan and helped that firm develop into one of many world’s main automakers.

Second, the corporate has made quite a few acquisitions, and presumably one of many standards driving these purchases was sturdy margins. Within the February 2024 presentation, nVent reported that it was constructing a robust observe document by specializing in high-growth verticals, new merchandise, and acquisitions.

Third, as a world participant, it’s well-positioned to optimize its sourcing, operations, and transportation.

Development

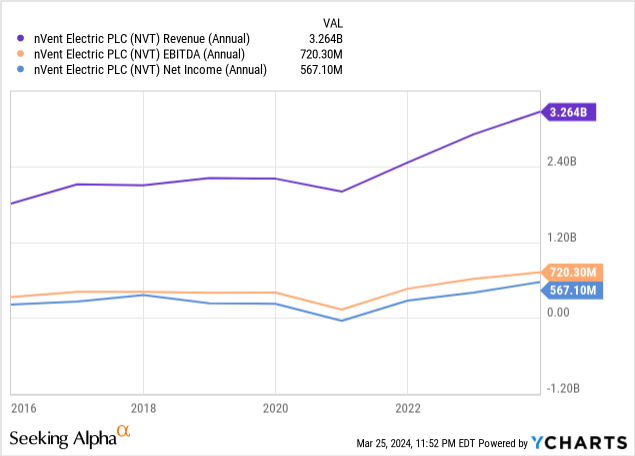

nVent has steadily grown its income, EBITDA, and web earnings since rising from the transient recession of 2020:

Observe that EBITDA and web earnings are usually not rising as quick as income, which makes me involved about the way forward for its margins. When backside line figures are usually not rising as rapidly as income, it suggests progress is turning into costlier.

What’s forward for progress? In its steering, issued with its fourth-quarter and full-year 2023 earnings, it forecast income progress of 8% to 10%. As for EPS, it expects $2.73 to $2.83 on a GAAP foundation and $3.17 to $3.27 on an adjusted foundation. Each earnings figures embrace successful of about $0.11 due to modifications in world tax requirements.

On an adjusted foundation, a rise from $3.06 for 2023 to $3.17 for 2024 would characterize a rise of three.6% and at $3.27, a 6.9% enhance.

Wall Road analysts lean towards the excessive facet of the 2024 adjusted steering:

NVT EPS Estimates desk (Looking for Alpha)

Final 12 months, nVent invested $71 million in capital expenditures, which ought to assist ship new progress. And as famous above, progress is within the firm’s DNA and a key part of the Our Sensible initiative.

It identified, within the February 2022 presentation, that it enjoys sturdy secular tailwinds. Particularly, it advantages from electrification, sustainability, and digitization traits, in addition to the Infrastructure Funding and Jobs Act.

Additional, it has what it calls “Large Development Alternatives, due to AI, vitality transition, and acquisition synergies.” It places its whole addressable market at $90 billion.

The corporate additionally has a rising dividend, which presently yields 1.03%, which is cheap for a progress firm. Its present payout ratio is 23.37% and its five-year progress price [CAGR] is 15.36%.

Administration and technique

CEO Beth Wozniak can also be Chair of the board of administrators and was President of Pentair’s Electrical phase earlier than the separation in 2018. Earlier than becoming a member of Pentair in 2015, she held management positions at Honeywell and its predecessor Allied Sign. Wozniak additionally serves as a director of Provider International Company (CARR) and Vice Chair of the Nationwide Electrical Producers Affiliation.

Sara Zawoyski has been Govt Vice President and Chief Monetary Officer since 2019. Beforehand she was a CFO in a number of world enterprise items and was vp of Investor Relations at Pentair. She began her profession at PricewaterhouseCoopers and likewise served in finance at PepsiAmericas (PEP).

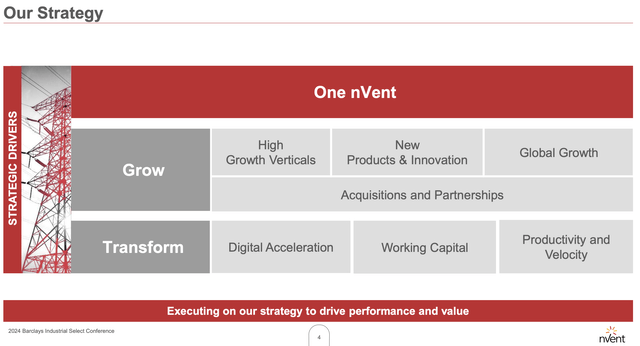

nVent laid out its enterprise technique on this slide from the February presentation:

NVT Enterprise Technique (February 2024 presentation)

It’s a method that is sensible, in that prime progress verticals, modern new merchandise, world progress and acquisitions/partnerships can all result in worthwhile, above-average progress.

The 2 most senior officers have the experience and expertise to drive new progress, as they’ve over the previous 5 years.

It additionally has free money move accessible to implement its technique; for 2023 it reported document money move efficiency, with FCF of $465 million.

nVent is a progress firm with the credentials, imaginative and prescient, and assets to maintain increasing.

Valuation

The ahead variations of valuation ratios point out nVent is modestly overvalued. The P/E Non-GAAP ratio is 22.65, which is 20.42% larger than the sector median. The P/E GAAP ratio is 22.65, some 22% above the sector median.

PEG Non-GAAP is 1.57, which is sort of 10% decrease than the Industrials median, and throughout the truthful worth vary. EV/EBITDA is excessive, at 16.13, properly above the sector median of 11.65. Worth/Gross sales is available in at 3.41, greater than double the median of 1.51. Equally, Worth/Ebook is 3.49 whereas the median is 2.76.

The Quant system offers a Maintain ranking, and the one different Looking for Alpha ranking clocks in as a Maintain. Of the 12 Wall Road analysts, 5 name it a Sturdy Purchase, three assess it as Purchase, and 4 have Maintain rankings.

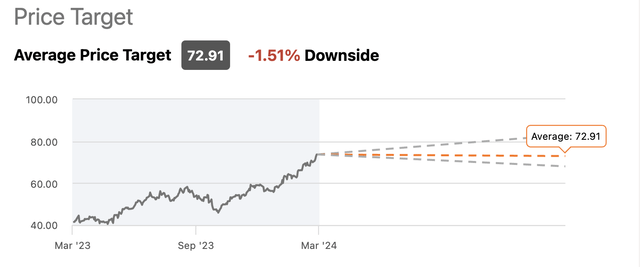

These Wall Road analysts are usually not collectively bullish, although. Their common value goal for one 12 months is $72.91, which is 1.51% under the closing value on March 25:

NVT Worth Targets (Looking for Alpha)

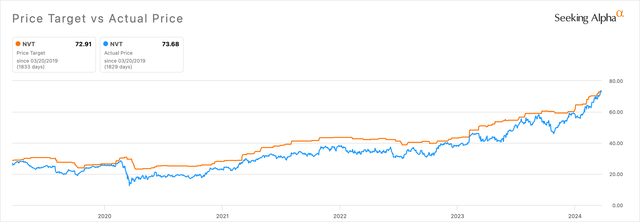

That appears counter-intuitive once we contemplate that the share value is up 78.51% over the previous 12 months (whereas EPS rose 42%, and adjusted EPS grew by 28%). But, the analysts have a superb document once we evaluate their targets and precise costs over the previous 5 years:

NVT Worth Targets vs Precise Costs (Looking for Alpha)

As we noticed above, they count on modest EPS progress this 12 months, 6.29%, adopted by will increase of 9.13% in 2025 and seven.97% in 2026.

Given nVent’s historical past of progress, its plans for acquisitions, and extra, I count on its share value to develop on the price of EPS progress moderately than on the analyst’s goal value (acknowledging they cowl barely completely different durations).

Including 6.29% to the March 25 closing value of $74.03 takes us to $78.69. That’s nowhere close to the value progress of final 12 months, however nonetheless extra promising than a discount. On the idea of that value and the corporate’s sturdy progress, I price nVent a Purchase.

Threat components

Financial and enterprise cycles might chew into its ongoing progress since demand for electrical merchandise decreases throughout a cycle’s downturn. Its finish markets embrace industrial, business and residential, infrastructure, and vitality markets, and all fluctuate.

nVent has develop into a world firm, exposing it to geopolitical and forex dangers. For instance, we noticed above that 2023’s EPS and adjusted EPS had been down due to forex points.

A few of its rivals are massive nationwide and world corporations that might be able to form markets in ways in which would possibly harm nVent. From the opposite facet, new corporations are stepping into these markets as properly (maybe partially due to the profitability of nVent), and a few attempt to broaden market share by slicing costs.

Acquisitions can pose issues for the acquisitor. It’s at all times a problem to combine a brand new agency into the fold, and failures might push up prices with out producing accretive income or earnings.

The latest 10-Ok reported that the corporate has been named as a defendant, goal, or doubtlessly accountable particular person in a number of environmental cleanup circumstances. As a result of it’s tough to understand how intensive potential clean-ups will likely be, additionally it is tough to know prematurely how a lot they’ll price.

Conclusion

nVent’s share value has been on a tear over the previous 12 months, as had been its earnings, albeit at completely different charges. The corporate’s steering for 2024 seems to be at 3.6% and 6.9% adjusted, and these estimates are in the identical vary as analyst EPS estimates of 6.29%.

The trajectory might have declined, however nVent stays a superb firm that ought to proceed to generate capital beneficial properties, most likely at a decrease price. Traders will even obtain a modest however rising dividend.

{kind=link}